Fill Out Your Maryland Tax 766 Template

Fill Out Your Maryland Tax 766 Template

When filling out the Maryland Tax 766 form, it’s important to follow certain guidelines to ensure everything is completed correctly. Here are seven things you should and shouldn't do:

By following these guidelines, you can help ensure that your tax withholding elections are processed smoothly and accurately.

Here are seven common misconceptions about the Maryland Tax 766 form, along with clarifications to help you understand the process better.

This form is invalid unless you provide your signature. Always ensure you sign before submission.

You must complete a combined form that covers both federal and state tax withholding elections. Each section must be filled out according to your preferences.

You must designate the number of withholding allowances on line 2 before entering any additional dollar amount on line 3.

If you are receiving payments from the Maryland State Retirement Agency, you still need to complete the form, even if you are not a resident.

You can change or revoke your withholding elections at any time by submitting a new form.

The Agency does not provide assistance with tax returns. For help, consult the IRS or a tax professional.

Failure to withhold enough federal or state taxes can lead to penalties. It's crucial to review your withholding choices regularly.

University of Maryland Requirements - Applicants should note the date, time, and contact information as part of the application process.

To access the necessary documentation for accurately filling out the Ohio Traffic Crash Report, you can visit Ohio PDF Forms, which provides useful resources that assist law enforcement and involved parties in the reporting process.

Md Form 510d - The form aids in calculating tax obligations for nonresident partners efficiently.

Filling out the Maryland Tax 766 form can be a straightforward process if you understand the key points. Here are some essential takeaways to keep in mind:

Completing the Maryland Tax 766 form requires careful attention to detail. This form is essential for establishing your federal and state tax withholding preferences related to your pension allowance. Follow these steps to ensure accurate completion.

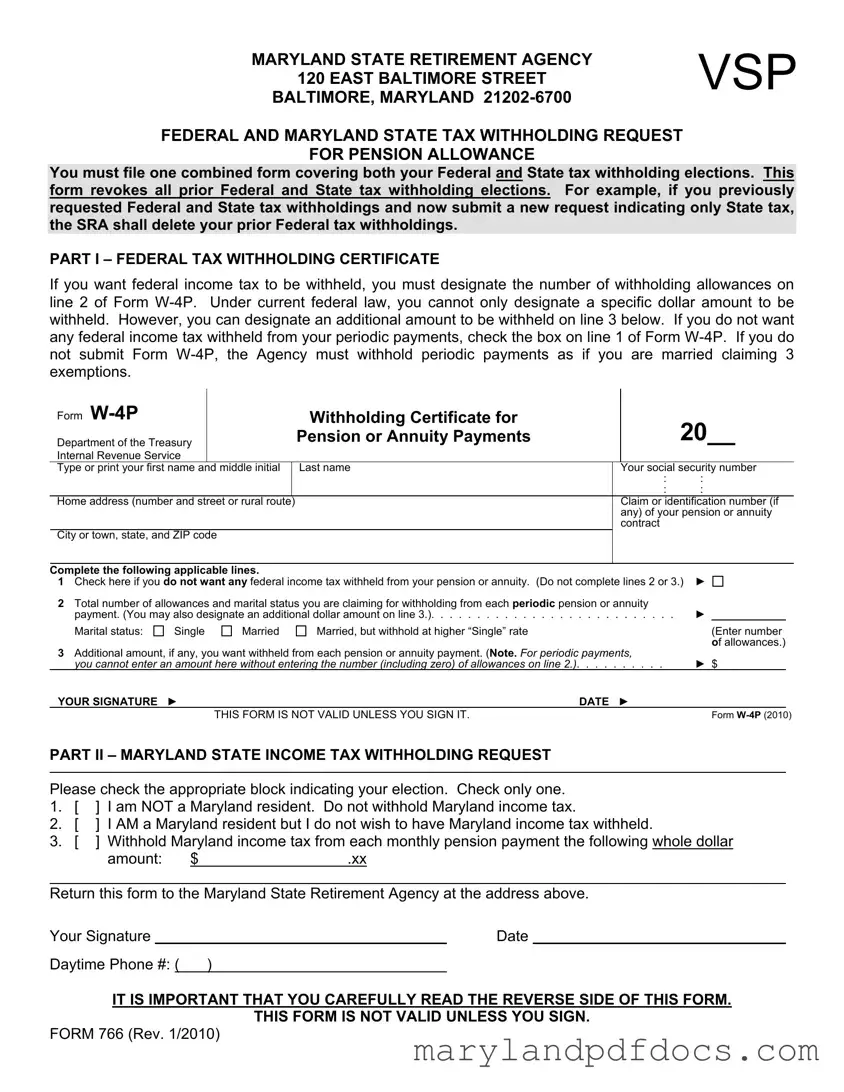

MARYLAND STATE RETIREMENT AGENCY |

VSP |

|

|

120 EAST BALTIMORE STREET |

|

BALTIMORE, MARYLAND |

|

FEDERAL AND MARYLAND STATE TAX WITHHOLDING REQUEST

FOR PENSION ALLOWANCE

You must file one combined form covering both your Federal and State tax withholding elections. This form revokes all prior Federal and State tax withholding elections. For example, if you previously requested Federal and State tax withholdings and now submit a new request indicating only State tax, the SRA shall delete your prior Federal tax withholdings.

PART I – FEDERAL TAX WITHHOLDING CERTIFICATE

If you want federal income tax to be withheld, you must designate the number of withholding allowances on line 2 of Form

Form |

|

|

|

Withholding Certificate for |

|

20__ |

|

||

Department of the Treasury |

|

|

Pension or Annuity Payments |

|

|

||||

|

|

|

|

|

|

|

|

||

Internal Revenue Service |

|

|

|

|

|

|

|

|

|

Type or print your first name and middle initial |

|

Last name |

|

Your social security number |

|||||

|

|

|

|

|

: |

: |

|

|

|

|

|

|

|

|

: |

: |

|

|

|

Home address (number and street or rural route) |

|

|

Claim or identification number (if |

||||||

|

|

|

|

|

|

any) of your pension or annuity |

|||

|

|

|

|

|

|

contract |

|

|

|

City or town, state, and ZIP code |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|||

Complete the following applicable lines. |

|

|

|

► |

|||||

1 Check here if you do not want any federal income tax withheld from your pension or annuity. (Do not complete lines 2 or 3.) |

|||||||||

2 Total number of allowances and marital status you are claiming for withholding from each periodic pension or annuity |

► |

|

|

||||||

payment. (You may also designate an additional dollar amount on line 3.) |

|||||||||

Marital status: |

Single |

Married |

Married, but withhold at higher “Single” rate |

|

|

(Enter number |

|||

|

|

|

|

|

|

|

|

of allowances.) |

|

3 Additional amount, if any, you want withheld from each pension or annuity payment. (Note. For periodic payments, |

► $ |

||||||||

you cannot enter an amount here without entering the number (including zero) of allowances on line 2.). . . . |

. . . . . . |

||||||||

YOUR SIGNATURE |

► |

|

|

DATE |

► |

|

|

|

|

|

|

THIS FORM IS NOT VALID UNLESS YOU SIGN IT. |

|

|

|

Form |

|||

PART II – MARYLAND STATE INCOME TAX WITHHOLDING REQUEST

Please check the appropriate block indicating your election. Check only one.

1.[ ] I am NOT a Maryland resident. Do not withhold Maryland income tax.

2.[ ] I AM a Maryland resident but I do not wish to have Maryland income tax withheld.

3.[ ] Withhold Maryland income tax from each monthly pension payment the following whole dollar

amount: |

$ |

.xx |

Return this form to the Maryland State Retirement Agency at the address above.

Your Signature |

|

|

Date |

|

Daytime Phone #: ( |

) |

|

||

|

|

|

|

|

IT IS IMPORTANT THAT YOU CAREFULLY READ THE REVERSE SIDE OF THIS FORM.

THIS FORM IS NOT VALID UNLESS YOU SIGN.

FORM 766 (Rev. 1/2010)

2

Part I

FEDERAL INCOME TAX WITHHOLDING

The monthly retirement payments you receive from the Maryland State Retirement and Pension System may be subject to Federal income tax withholding. For further information, please refer to Internal Revenue Service Publication 575 regarding the taxability of pension and annuity income.

As a retiree, the following Federal income tax withholding alternatives are available to you:

1.You may elect not to have Federal income tax deducted from your monthly retirement payment, or

2.You may claim a certain number of exemptions and have the Maryland State Retirement and Pension System deduct the appropriate amount, if any, in accordance with the Federal income tax tables and you may designate an additional specific whole dollar amount to be withheld from your monthly retirement payment.

If you elect not to have Federal withholding apply to your monthly retirement payments, or if you do not have enough Federal income tax withheld, you may be responsible for payment of estimated tax. You may incur penalties under the Internal Revenue Service estimated tax rules if your withholding and estimated tax payment are not sufficient. New retirees, especially, should see IRS Publication 505.

Part II

MARYLAND STATE INCOME TAX WITHHOLDING

The monthly retirement payments you receive from the Maryland State Retirement and Pension System may be subject to Maryland income tax withholding.

As a retiree and a Maryland resident, the following Maryland income tax withholding alternatives are available to you:

1.You may elect not to have Maryland income tax deducted from your monthly retirement payment, or

2.You may designate a specific whole dollar amount to be withheld from your monthly retirement payment.

If you elect not to have Maryland withholding apply to your monthly retirement payments, or if you do not have enough Maryland income tax withheld, you may be responsible for payment of estimated tax.

An election of any one of the alternatives will remain in effect until you revoke it. You may revoke or change your election at any time by filing a new Federal and Maryland State Tax Withholding Request.

The Maryland State Retirement Agency can not assist you in the preparation of tax returns. Please contact the Internal Revenue Service at

To receive additional copies of the Federal and Maryland State Tax Withholding Request form, or for other information concerning your retirement benefits, call

SEE REVERSE SIDE FOR FEDERAL AND MARYLAND STATE TAX WITHHOLDING REQUEST

FORM 766 (Rev. 1/2010)

Additional Instructions:

Section references are to the Internal Revenue Code. Agency refers to the Maryland State Retirement Agency.

When should I complete the form? Complete Form

Other income. If you have a large amount of income from other sources not subject to withholding (such as interest, dividends, or capital gains), consider making estimated tax payments using Form

Withholding From Pensions and Annuities

Generally, federal income tax withholding applies to the taxable part of payments made from pension,

Because your tax situation may change from year to year, you may want to refigure your withholding each year. You can change the amount to be withheld by using lines 2 and 3 of Form

Choosing not to have income tax withheld. You (or in the event of death, your beneficiary or estate) can choose not to have federal income tax withheld from your payments by using line 1 of Form

Caution. There are penalties for not paying enough federal income tax during the year, either through withholding or estimated tax payments. New retirees, especially, should see Pub. 505. It explains your estimated tax requirements and describes penalties in detail. You may be able to avoid quarterly estimated tax payments by having enough tax withheld from your pension or annuity using Form

Periodic payments. Withholding from periodic payments of a pension or annuity is figured in the same manner as withholding from wages. Periodic payments are made in installments at regular intervals over a period of more than 1 year. They may be paid annually, quarterly, monthly, etc.

If you want federal income tax to be withheld, you must designate the number of withholding allowances on line 2 of Form

3

designate an additional amount to be withheld on line 3. If you do not want any federal income tax withheld from your periodic payments, check the box on line 1 of Form

Caution. If you do not submit Form

If you submit a Form

taxpayer identification number (TIN), the payer must withhold as if you are single claiming zero withholding allowances even if you choose not to have federal income tax withheld.

There are some kinds of periodic payments for which you cannot use Form

For periodic payments, your Form

Changing Your “No Withholding” Choice

Periodic Payments. If you previously chose not to have federal income tax withheld and you now want withholding, complete another Form

Payments to Foreign Persons and

Payments Outside the United States

Unless you are a nonresident alien, withholding (in the manner described above) is required on any periodic or nonperiodic payments that are delivered to you outside the United States or its possessions. You cannot choose not to have federal income tax withheld on line 1 of Form

In the absence of a tax treaty exemption, nonresident aliens, nonresident alien beneficiaries, and foreign estates generally are subject to a 30% federal withholding tax under section 1441 on the taxable portion of a periodic or nonperiodic pension or annuity payment that is from U.S. sources. However, most tax treaties provide that private pensions and annuities are exempt from withholding and tax. Also, payments from certain pension plans are exempt from withholding even if no tax treaty applies. See Pub.

Statement of Federal Income Tax Withheld From Your Pension or Annuity

By January 31 of next year, your payer will furnish a statement to you on Form

Not Signing the Form: A common mistake is failing to sign the Maryland Tax 766 form. Without your signature, the form is invalid and cannot be processed.

Incorrectly Filling Out Personal Information: Ensure that your name, Social Security number, and address are accurate. Any errors can lead to processing delays.

Choosing the Wrong Residency Status: Carefully check the box that reflects your residency status. Misidentifying yourself as a non-resident when you are a resident can lead to incorrect tax withholding.

Leaving Out Allowances: When filling out the Federal Tax Withholding section, you must indicate the number of allowances you are claiming. Failing to do so will result in default withholding, which may not suit your financial situation.

Not Designating an Additional Amount: If you want an extra amount withheld, you must specify this on line 3. Omitting this can lead to insufficient withholding.

Ignoring the Instructions: It is crucial to read all instructions provided on the form. Overlooking important details can result in errors that affect your tax situation.

Failing to Submit the Form Promptly: Delay in submitting the form can affect your tax withholding for the year. It is best to send it as soon as possible to avoid complications.

Not Keeping a Copy: Always retain a copy of the completed form for your records. This can be helpful for future reference or in case of discrepancies.

What is the Maryland Tax 766 form?

The Maryland Tax 766 form, also known as the Federal and Maryland State Tax Withholding Request for Pension Allowance, is a document used by retirees to specify their federal and state tax withholding preferences. This form must be submitted to the Maryland State Retirement Agency and covers both federal and Maryland state tax elections. It revokes any previous withholding elections, ensuring that the most current choices are in effect.

Who needs to complete the Maryland Tax 766 form?

Retirees receiving pension or annuity payments from the Maryland State Retirement and Pension System should complete this form. It is particularly important for those who wish to adjust their federal and state tax withholding amounts or for those who are newly retired and need to establish their withholding preferences.

What information is required on the form?

The form requires personal information, including your name, Social Security number, home address, and claim or identification number related to your pension or annuity. Additionally, you will need to indicate your federal tax withholding preferences by completing Form W-4P, which includes your marital status and the number of allowances you wish to claim. For Maryland state tax withholding, you will specify whether you are a resident and if you want state taxes withheld from your pension payments.

Can I choose not to have any federal income tax withheld?

Yes, if you do not wish to have federal income tax withheld from your pension or annuity payments, you can indicate this by checking the appropriate box on line 1 of Form W-4P. However, if you do not submit this form, the agency will withhold taxes as if you are married claiming three exemptions, which may not align with your actual tax situation.

What are the options for Maryland state tax withholding?

For Maryland state tax withholding, you have several options. You can choose not to have any Maryland income tax withheld, or if you are a Maryland resident, you can specify a whole dollar amount to be withheld from each monthly pension payment. Your choice will remain in effect until you decide to change or revoke it by submitting a new withholding request.

What happens if I do not submit the form?

If you fail to submit the Maryland Tax 766 form, the Maryland State Retirement Agency will withhold taxes based on default assumptions. This means that your withholding will be calculated as if you are married and claiming three exemptions, which may lead to an unexpected tax liability at the end of the year. It is essential to complete and submit the form to ensure your withholding aligns with your financial situation.

How often can I change my withholding preferences?

You can change your withholding preferences at any time by submitting a new Maryland Tax 766 form. This flexibility allows you to adjust your elections based on changes in your financial circumstances, tax liabilities, or personal preferences. It is advisable to review your withholding annually or whenever your financial situation changes.

Where should I send the completed form?

Once you have completed the Maryland Tax 766 form, you should return it to the Maryland State Retirement Agency at the address listed on the form: 120 East Baltimore Street, Baltimore, Maryland 21202-6700. Ensure that you sign the form, as it is not valid without your signature.