Fill Out Your Maryland Frorm 510 Template

Fill Out Your Maryland Frorm 510 Template

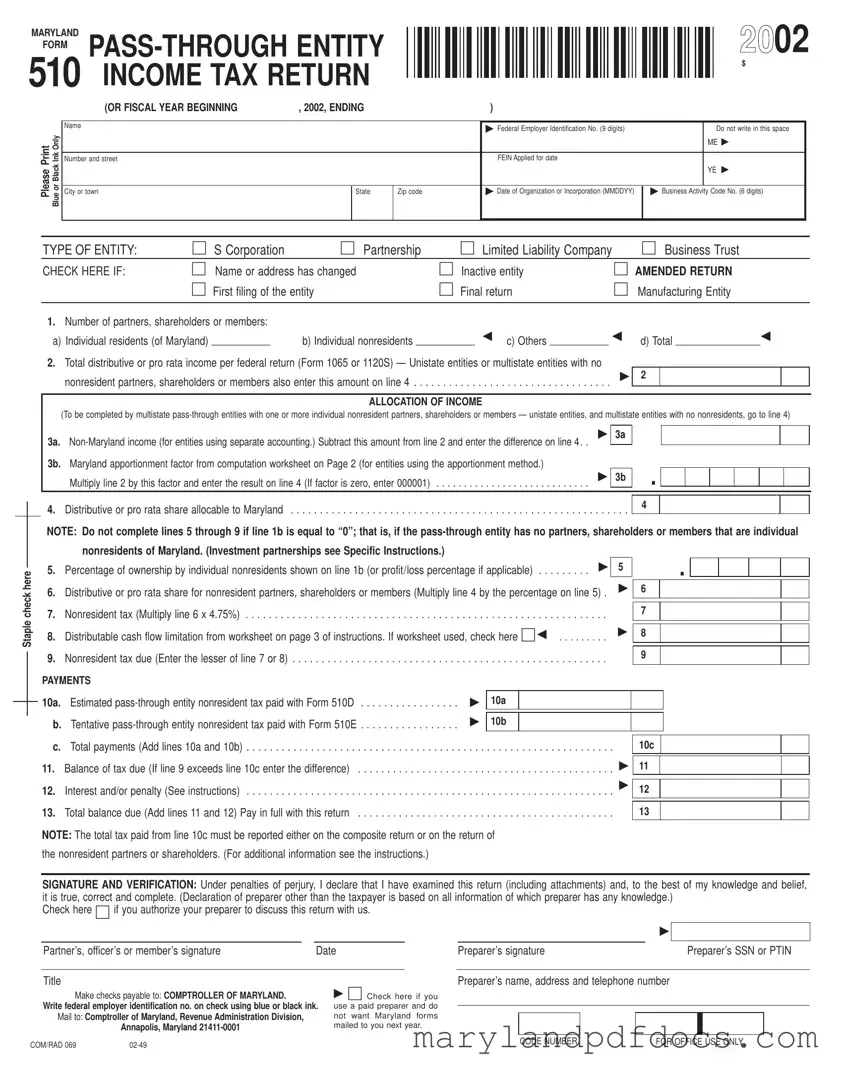

When completing the Maryland Form 510, there are several important dos and don'ts to keep in mind. This will help ensure that your submission is accurate and complete, minimizing the risk of delays or issues with your tax return.

Referral Request Form - It helps streamline the process of specialist consultations within the healthcare system.

When drafting legal documents, utilizing a reliable template for a Non-disclosure Agreement form can save time and ensure all necessary clauses are included, thereby safeguarding sensitive information effectively.

State of Maryland Insurance - Optometrists and ophthalmologists complete this form for vision service claims.

Filling out the Maryland Form 510 is an important step for pass-through entities. Here are some key takeaways to keep in mind:

Taking the time to understand these key points can help streamline the filing process and ensure compliance with Maryland tax regulations.

Completing the Maryland Form 510 requires careful attention to detail. This form is essential for pass-through entities, such as S Corporations and Partnerships, to report income and taxes. Follow the steps outlined below to ensure accurate completion of the form.

After completing these steps, review the form for accuracy. It is essential to ensure that all information is correct before submitting to avoid delays or issues with your tax return.

MARYLAND

FORM

2002

$

|

(OR FISCAL YEAR BEGINNING |

, 2002, ENDING |

|

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

▶ Federal Employer Identification No. (9 digits) |

|

Do not write in this space |

|

|

|

|

|

|

|

|

||

PrintPlease InkBlackorBlueOnly |

|

|

|

|

|

|

ME ▶ |

|

|

|

|

|

|

|

|

|

|

Number and street |

|

|

|

FEIN Applied for date |

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

YE ▶ |

|

|

|

|

|

|

|

|

|

|

|

City or town |

|

State |

Zip code |

▶ Date of Organization or Incorporation (MMDDYY) |

▶ Business Activity Code No. (6 digits) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Staple check here

TYPE OF ENTITY: |

☐ S Corporation |

☐ Partnership |

☐ Limited Liability Company |

☐ Business Trust |

CHECK HERE IF: |

☐ Name or address has changed |

☐ Inactive entity |

☐ AMENDED RETURN |

|

|

☐ First filing of the entity |

☐ Final return |

☐ Manufacturing Entity |

|

|

|

|

|

|

1. Number of partners, shareholders or members: |

|

|

|

|

a) Individual residents (of Maryland) ___________ |

b) Individual nonresidents ___________ ◀ c) Others ___________ ◀ d) Total ________________◀ |

|||

2.Total distributive or pro rata income per federal return (Form 1065 or 1120S) Ñ Unistate entities or multistate entities with no

▶ 2 nonresident partners, shareholders or members also enter this amount on line 4 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

ALLOCATION OF INCOME |

|

|

|

(To be completed by multistate |

|||

|

▶ |

3a |

|

3a. |

|

|

|

3b. Maryland apportionment factor from computation worksheet on Page 2 (for entities using the apportionment method.) |

|

|

|

|

▶ |

3b |

|

Multiply line 2 by this factor and enter the result on line 4 (If factor is zero, enter 000001) |

|

|

. |

|

|

|

4 |

4. Distributive or pro rata share allocable to Maryland |

. . . |

. . . . . |

. |

NOTE: Do not complete lines 5 through 9 if line 1b is equal to “0”; that is, if the

|

|

|

|

|

|

|

|

5 |

|

. |

|

|

|

|

5. |

Percentage of ownership by individual nonresidents shown on line 1b (or profit/loss percentage if applicable) |

▶ |

|

|

|

|

|

|

||||||

. . . |

|

|

|

|

|

|

|

|||||||

6. |

Distributive or pro rata share for nonresident partners, shareholders or members (Multiply line 4 by the percentage on line 5) . |

|

▶ |

6 |

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7. |

Nonresident tax (Multiply line 6 x 4.75%) |

|

|

|

|

|

|

|

7 |

|

|

|

|

|

. . . |

. |

. . . . . |

. . . . . . . . . . . . |

. . . |

|

|

|

|

|

|

|

|

||

8. |

Distributable cash flow limitation from worksheet on page 3 of instructions. If worksheet used, check here ☐ ◀ |

|

|

▶ |

8 |

|

|

|

|

|

||||

. . . |

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9. |

Nonresident tax due (Enter the lesser of line 7 or 8) |

|

|

|

|

|

|

|

9 |

|

|

|

|

|

. . . |

|

. . . . . |

. . . . . . . . . . . . |

. . . |

|

|

|

|

|

|

|

|

||

PAYMENTS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10a. |

Estimated |

▶ |

|

10a |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

b. |

Tentative |

▶ |

|

10b |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

c. |

Total payments (Add lines 10a and 10b) |

. . . |

|

. . . . . . |

. . . . . . . . . . . . |

. . . |

. |

10c |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

11. |

Balance of tax due (If line 9 exceeds line 10c enter the difference) |

. . . |

|

. . . . . . |

. . . . . . . . . . . . |

. . . |

. |

▶ |

11 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12. |

Interest and/or penalty (See instructions) |

|

|

|

|

|

|

▶ |

12 |

|

|

|

|

|

. . . |

|

. . . . . . |

. . . . . . . . . . . . |

. . . |

. |

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13. |

Total balance due (Add lines 11 and 12) Pay in full with this return |

. . . |

|

. . . . . . |

. . . . . . . . . . . . |

. . . |

. |

13 |

|

|

|

|

|

|

NOTE: The total tax paid from line 10c must be reported either on the composite return or on the return of |

|

|

|

|

|

|

|

|

|

|||||

the nonresident partners or shareholders. (For additional information see the instructions.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SIGNATURE AND VERIFICATION: Under penalties of perjury, I declare that I have examined this return (including attachments) and, to the best of my knowledge and belief, it is true, correct and complete. (Declaration of preparer other than the taxpayer is based on all information of which preparer has any knowledge.)

Check here ☐ if you authorize your preparer to discuss this return with us.

|

PartnerÕs, officerÕs or memberÕs signature |

Date |

|||

|

|

|

|

|

|

|

Title |

|

|

▶ ☐ Check here if you |

|

|

Make checks payable to: COMPTROLLER OF MARYLAND. |

|

|||

|

Write federal employer identification no. on check using blue or black ink. |

use a paid preparer and do |

|||

|

Mail to: Comptroller of Maryland, Revenue Administration Division, |

|

not want Maryland forms |

||

|

|

Annapolis, Maryland |

|

mailed to you next year. |

|

COM/RAD 069 |

|

|

|

||

|

|

|

|

◀ |

|

|

|

|

|

|

|

|

|

|

|

|

|

PreparerÕs signature |

|

PreparerÕs SSN or PTIN |

||||||

|

|

|

|

|

|

|

|

|

PreparerÕs name, address and telephone number |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CODE NUMBER |

FOR OFFICE USE ONLY |

||||||

MARYLAND |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FORM 510 |

INCOME TAX RETURN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2002 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PAGE 2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

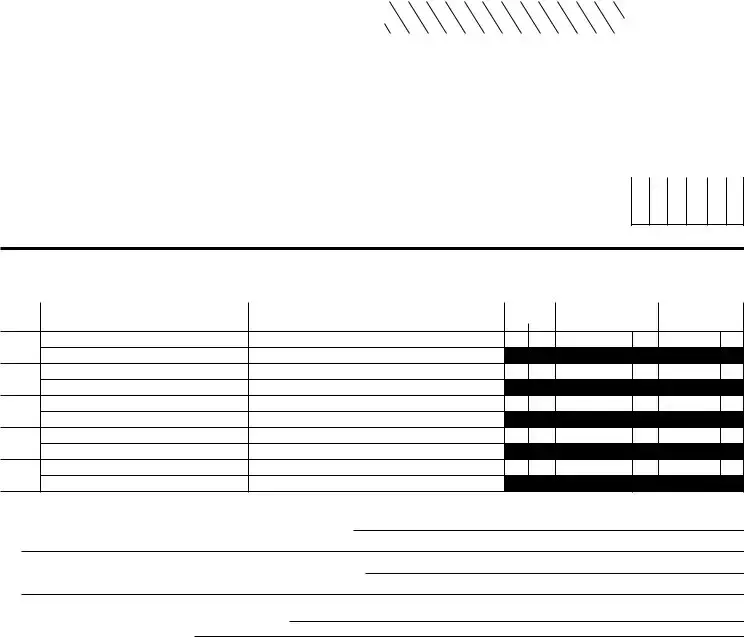

COMPUTATION OF APPORTIONMENT FACTOR |

|

|

|

|

|

|

|

|

Column 1 |

|

|

|

|

|

|

|

|

|

Column 2 |

|

|

|

|

|

|

|

Column 3 |

|||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

TOTALS |

|

|

|

|

|

|

|

|

|

TOTALS |

|

DECIMAL FACTOR |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||

(Applies only to multistate |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

WITHIN |

|

|

|

|

|

WITHIN AND |

|

|

|

Column 1 Ö Column 2 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||

NOTE: Special apportionment formulas are required for rental/leasing, transportation and |

|

|

|

|

|

|

MARYLAND |

|

|

|

|

|

|

|

|

WITHOUT |

( rounded to six places ) |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

manufacturing companies. Multistate manufacturers with more than 25 employees |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

MARYLAND |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

must complete Form 500MC. See Instructions. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1A. Receipts |

a. Gross receipts or sales less returns and allowances . . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

b. Dividends |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

c. Interest |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

d. Gross rents |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

e. Gross royalties |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

f. Capital gain net income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

g. Other income (Attach schedule) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

1B. Receipts |

h. Total receipts (Add lines 1A(a) through 1A(g), for Columns 1 and 2) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

(Enter the same factor shown on line 1A, Column 3 Ð Disregard this line if |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

2. Property |

special apportionment formula used.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

a. Inventory |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

b. Machinery and equipment |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

c. Buildings |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

d. Land |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

e. Other tangible assets (Attach schedule) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

f. Rent expense capitalized (multiplied by eight) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

3. Payroll |

g. Total property (Add lines 2a through 2f, for Columns 1 and 2) . . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

a. Compensation of officers |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

b. Other salaries and wages |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

c. Total payroll (Add lines 3a and 3b, for Columns 1 and 2) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

4. Total of factors (Add entries in Column 3) |

. |

. |

|

. |

. |

. |

. |

|

. |

. |

|

. |

. |

. |

. . |

|

. |

. |

. |

|

. |

. |

|

. |

. |

. |

. |

|

. |

. |

. |

. |

. |

. |

|

. |

. |

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

5.Maryland apportionment factor (Divide line 4 by four for

PARTNERS’, SHAREHOLDERS’ OR MEMBERS’ INFORMATION (Attach continuing schedule in same format if there are more than five partners, shareholders or members)

Name and social security number or federal |

Address |

Check here |

Distributive or |

Distributive or |

employer identification number |

|

if Maryland: |

pro rata share of income |

pro rata share of tax paid |

|

Non- |

(See Instructions) |

(See Instructions) |

|

|

|

Resident resident |

|

|

1

2

3

4

5

ADDITIONAL INFORMATION REQUIRED (Attach a separate schedule if more space is necessary)

1.Address of principal place of business (if other than indicated on page 1):

2.Address at which tax records are located (if other than indicated on page 1):

3.Telephone number of

4.State of organization or incorporation:

5.Has the Internal Revenue Service made adjustments (for a tax year in which a Maryland return was required) that were not previously reported

to the Maryland Revenue Administration Division? |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ☐ Yes |

☐ No |

|

If Òyes,Ó indicate tax year(s) here: |

|

and submit an amended return(s) together with a copy of the IRS adjustment report(s) |

|

under separate cover. |

|

|

|

6. Did the |

☐ No |

||

COM/RAD 069 |

Incorrect Entity Type Selection: Failing to accurately select the type of entity (S Corporation, Partnership, Limited Liability Company, or Business Trust) can lead to significant issues. Each entity type has different tax obligations, and selecting the wrong one can result in incorrect filings.

Missing or Incorrect Identification Numbers: Not providing the Federal Employer Identification Number (FEIN) or entering it incorrectly is a common mistake. This number is crucial for processing the return and linking it to the correct entity.

Errors in Income Reporting: Misreporting the total distributive or pro rata income from the federal return can cause discrepancies. Ensure that the amounts from Form 1065 or 1120S are accurately reflected on the Maryland Form 510.

Neglecting Nonresident Partner Information: If there are individual nonresident partners, shareholders, or members, failing to complete the relevant lines can result in penalties. It is essential to report their ownership percentages and calculate their distributive shares correctly.

What is the Maryland Form 510?

The Maryland Form 510 is an income tax return specifically designed for pass-through entities, such as S corporations, partnerships, limited liability companies, and business trusts. This form is used to report income, deductions, and tax liabilities for these entities. It ensures that the income is appropriately allocated to partners, shareholders, or members, especially when they include nonresidents of Maryland.

Who needs to file the Maryland Form 510?

If your business operates as a pass-through entity and has partners, shareholders, or members, you will likely need to file the Maryland Form 510. This includes S corporations, partnerships, and limited liability companies. If your entity has any nonresident partners or shareholders, filing this form becomes even more crucial to ensure proper tax compliance.

When is the Maryland Form 510 due?

The due date for the Maryland Form 510 typically aligns with the federal tax return deadlines. For calendar year filers, this means the form is due on April 15. If your entity operates on a fiscal year basis, the form is due on the 15th day of the fourth month following the end of your fiscal year. Always check for any updates or changes in deadlines that may occur.

What information do I need to complete the Maryland Form 510?

To complete the Maryland Form 510, you will need several pieces of information, including the entity's name, Federal Employer Identification Number (FEIN), and business activity code. Additionally, you should gather details about your partners, shareholders, or members, including their residency status and distributive shares of income. If applicable, you will also need to calculate your Maryland apportionment factor, especially if your entity operates in multiple states.

How do I determine the distributive share for nonresident partners?

The distributive share for nonresident partners is calculated by multiplying the total income allocable to Maryland by the percentage of ownership held by the nonresident partners. This ensures that nonresidents only pay taxes on their share of income earned within Maryland. If you have questions about how to accurately make these calculations, consider seeking guidance from a tax professional.

What happens if I miss the filing deadline for Form 510?

If you miss the filing deadline for the Maryland Form 510, your entity may be subject to penalties and interest on any unpaid taxes. It's essential to file as soon as possible, even if you cannot pay the full amount owed. Consider reaching out to the Maryland Revenue Administration Division to discuss your situation and explore options for compliance.

Can I amend my Maryland Form 510 after filing?

Yes, you can amend your Maryland Form 510 if you discover errors or need to make changes after the initial filing. To do this, you will need to indicate that the return is amended and provide the corrected information. It’s important to submit any necessary documentation along with the amended return to ensure accurate processing.