Fill Out Your Maryland Cof 85 Template

Fill Out Your Maryland Cof 85 Template

When filling out the Maryland Cof 85 form, it is essential to approach the task with care and attention to detail. Here are seven important do's and don'ts to guide you through the process:

By following these guidelines, you can confidently complete the Maryland Cof 85 form, ensuring that your organization remains compliant and transparent in its financial reporting.

Misconceptions about the Maryland Cof 85 form can lead to confusion among organizations required to file it. Below are eight common misconceptions, along with clarifications for each.

This form is applicable to all organizations that do not file Form 990, regardless of their size. Smaller organizations often overlook this requirement.

In Maryland, organizations that meet specific criteria must file the Cof 85 form annually. Failure to do so can result in penalties.

While both forms are financial disclosures, the Cof 85 form is specifically designed for organizations that do not file Form 990. It has different requirements and sections.

Any organization that meets the filing criteria, including certain for-profit entities, may be required to submit the Cof 85 form.

The form requires comprehensive financial data, including revenue, expenses, and changes in net assets. Organizations must provide accurate and detailed information.

Organizations must adhere to specific deadlines for filing the Cof 85 form, typically aligned with their fiscal year-end. Missing the deadline can lead to penalties.

The form is subject to review by the state, regardless of whether issues arise. Accurate filing is essential to maintain compliance.

Organizations must update the Cof 85 form annually to reflect their current financial situation. Any significant changes in operations or finances should also be reported.

Tangible Net Benefit - Borrowers need to track all aspects of costs associated with new loans.

Among the key steps in the homeschooling process is the submission of the Virginia Homeschool Letter of Intent, a vital form for parents intending to educate their children at home. This document serves to officially inform the local school division about the family's decision, ensuring compliance with state regulations. For those looking to simplify this process, templates and guidelines are available at homeschoolintent.com/editable-virginia-homeschool-letter-of-intent, which can be invaluable in crafting a thorough and compliant letter.

Maryland Traffic Ticket Lookup - The citation number is conveniently printed beneath the bar code on your citation.

When filling out and using the Maryland COF-85 form, organizations should keep the following key takeaways in mind:

Filling out the Maryland Cof 85 form requires attention to detail and accurate information about your organization’s finances. Follow these steps to complete the form correctly.

Once the form is completed, review it for accuracy and ensure all required attachments are included. Submit the form as directed by the Maryland Secretary of State’s office.

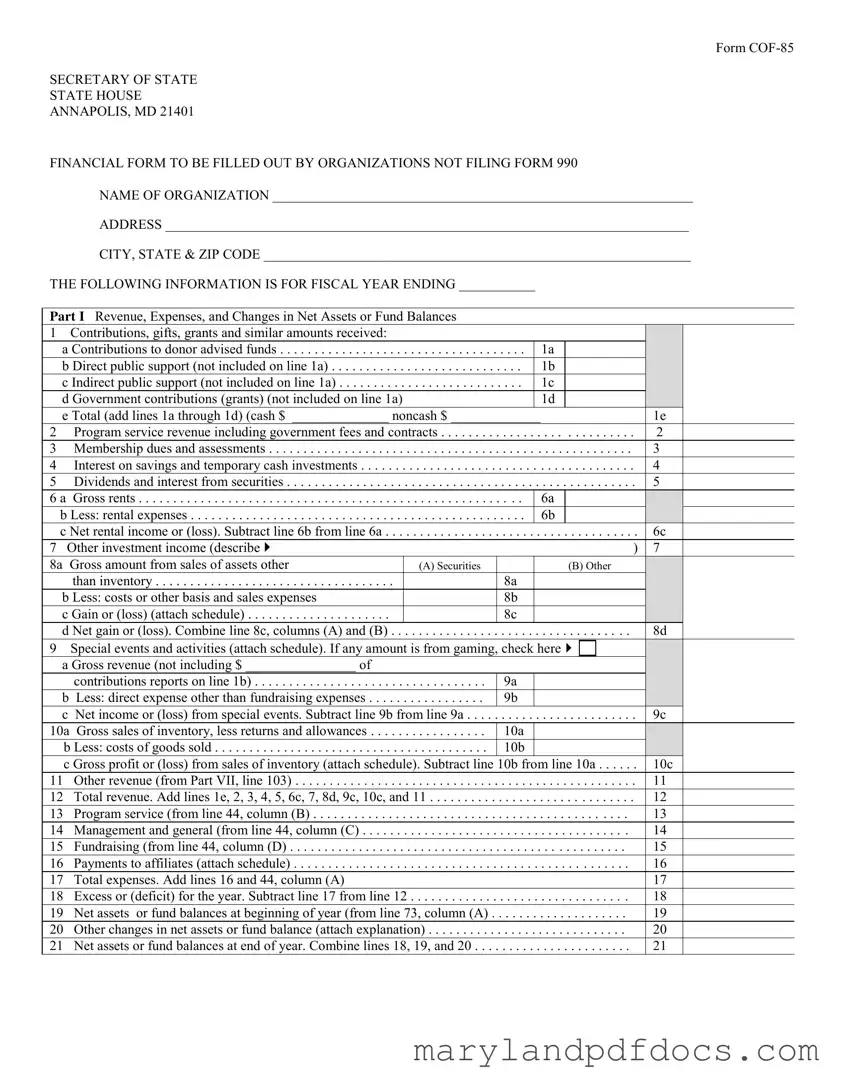

Form

SECRETARY OF STATE

STATE HOUSE

ANNAPOLIS, MD 21401

FINANCIAL FORM TO BE FILLED OUT BY ORGANIZATIONS NOT FILING FORM 990

NAME OF ORGANIZATION _____________________________________________________________

ADDRESS ____________________________________________________________________________

CITY, STATE & ZIP CODE ______________________________________________________________

THE FOLLOWING INFORMATION IS FOR FISCAL YEAR ENDING ___________

Part I Revenue, Expenses, and Changes in Net Assets or Fund Balances

1 Contributions, gifts, grants and similar amounts received: |

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|||

a Contributions to donor advised funds |

. . . . . . . . . . . . |

. . . . |

1a |

|

|

|

|

|

|

|

||

b Direct public support (not included on line 1a) |

. . . . |

1b |

|

|

|

|

|

|

|

|||

c Indirect public support (not included on line 1a) |

. . . . |

1c |

|

|

|

|

|

|

|

|||

d Government contributions (grants) (not included on line 1a) |

|

|

1d |

|

|

|

|

|

|

|

||

e Total (add lines 1a through 1d) (cash $ ______________ noncash $ _____________ |

|

|

|

|

1e |

|

||||||

2 Program service revenue including government fees and contracts |

. . . . . |

. . . . |

. . |

. . |

. . . . . . |

2 |

|

|

||||

3 Membership dues and assessments |

. . . . . . . . . . . . |

. . . . . |

. . . . |

. . |

. . . |

. . . . . |

3 |

|

|

|||

4 Interest on savings and temporary cash investments |

. . . . . . |

. . . . |

. . |

. . |

. . . . . . |

4 |

|

|

||||

5 Dividends and interest from securities |

. . . . . . . . . . . . |

. . . . . |

. . . . . |

. . |

. . |

. . . . . . |

5 |

|

|

|||

6 a |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Gross rents |

. . . . |

6a |

|

|

|

|

|

|

|

||

b Less: rental expenses |

. . . . . . . . . . . . |

. . . . |

6b |

|

|

|

|

|

|

|

||

c Net rental income or (loss). Subtract line 6b from line 6a |

. . . . . . . . . . . . |

. . . . . |

. . . . . |

. . |

. . |

. . . . . . |

6c |

|

||||

7 Other investment income (describe |

|

) |

7 |

|

|

|||||||

8a |

Gross amount from sales of assets other |

|

(A) Securities |

|

|

(B) Other |

|

|

|

|

||

|

than inventory |

|

|

8a |

|

|

|

|

|

|

|

|

b Less: costs or other basis and sales expenses |

|

|

8b |

|

|

|

|

|

|

|

||

c Gain or (loss) (attach schedule) |

|

|

8c |

|

|

|

|

|

|

|

||

d Net gain or (loss). Combine line 8c, columns (A) and (B) . . |

. . |

. . . . . . . . . . . . |

. . . . . |

. . . . . |

. . |

. . |

. . . . . |

8d |

|

|||

9 |

Special events and activities (attach schedule). If any amount is from gaming, check here |

|

|

|

|

|

|

|||||

a Gross revenue (not including $ ________________ of |

|

|

|

|

|

|

|

|

|

|

||

|

contributions reports on line 1b) |

. . . . . . . . . . |

9a |

|

|

|

|

|

|

|

||

b |

Less: direct expense other than fundraising expenses |

9b |

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

||||

c |

Net income or (loss) from special events. Subtract line 9b from line 9a |

. . . . . |

. . . . . |

. . |

. . |

. . . . . . |

9c |

|

||||

10a |

. . . . . . .Gross sales of inventory, less returns and allowances |

. . . . . . . . . . |

10a |

|

|

|

|

|

|

|

||

b Less: costs of goods sold |

10b |

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

||||||

c Gross profit or (loss) from sales of inventory (attach schedule). Subtract line |

10b from line 10a |

10c |

|

|||||||||

11 |

Other revenue (from Part VII, line 103) |

. . . . . . . . . . . . |

. . . . . |

. . . . . |

. . |

. . |

. . . . . . |

11 |

|

|

||

12 |

Total revenue. Add lines 1e, 2, 3, 4, 5, 6c, 7, 8d, 9c, 10c, and 11 |

. . . . . . |

. . . . |

. . |

. . |

. . . . . . |

12 |

|

|

|||

13 |

Program service (from line 44, column (B) |

. . . . . . |

. . . . |

. . |

. . . |

. . . . |

13 |

|

|

|||

14 |

Management and general (from line 44, column (C) |

. . . . . |

. . . . . |

. . |

. . |

. . . . . |

14 |

|

|

|||

15 |

Fundraising (from line 44, column (D) |

. . . . . . |

. . . . |

. . |

. . . |

. . . . |

15 |

|

|

|||

16 |

Payments to affiliates (attach schedule) |

. . . . . |

. . |

. . |

. . . . . |

16 |

|

|

||||

17 |

Total expenses. Add lines 16 and 44, column (A) |

|

|

|

|

|

|

17 |

|

|

||

18 |

Excess or (deficit) for the year. Subtract line 17 from line 12 |

. . . . . |

. . . . . |

. . |

. . |

. . . . . |

18 |

|

|

|||

19 |

Net assets or fund balances at beginning of year (from line 73, column (A) . |

. . . . . . |

. . . . |

. . |

. . . |

. . . . |

19 |

|

|

|||

20 |

Other changes in net assets or fund balance (attach explanation) |

. . . . . . |

. . . . |

. . |

. . . |

. . . . |

20 |

|

|

|||

21 |

Net assets or fund balances at end of year. Combine lines 18, 19, and 20 . . . . |

. . . . . |

. . . . . |

. . |

. . |

. . . . . |

21 |

|

|

|||

|

|

|

|

|

Page 2 |

PART II STATEMENT OF FUNCTIONAL EXPENSES |

|

|

|

|

|

|

|

|

|

|

|

Do not include amounts reported on lines |

(A) Total |

(B) Program |

(C) Management |

(D) |

|

6(b), 8(b), 9(b), 10(b), or 16 of Part 1. |

|

services |

and general |

Fundraising |

|

22 |

Grants and allocations (attach schedule) |

|

|

|

|

23 |

Specific assistance to individuals |

|

|

|

|

24 |

Benefits paid to or for members |

|

|

|

|

25 |

Compensation of officers, directors, etc |

|

|

|

|

26 |

Other salaries and wages |

|

|

|

|

27 |

Pension plan contributions |

|

|

|

|

28 |

Other employee benefits |

|

|

|

|

29 |

Payroll taxes |

|

|

|

|

30 |

Professional fundraising fees |

|

|

|

|

31 |

Accounting fees |

|

|

|

|

32 |

Legal fees |

|

|

|

|

33 |

Supplies |

|

|

|

|

34 |

Telephone |

|

|

|

|

35 |

Postage and shipping |

|

|

|

|

36 |

Occupancy |

|

|

|

|

37 |

Equipment rental and maintenance |

|

|

|

|

38 |

Printing and publications |

|

|

|

|

39 |

Travel |

|

|

|

|

40 |

Conferences, conventions and meetings |

|

|

|

|

41 |

Interest |

|

|

|

|

42 Depreciation, depletion, etc. (attach schedule) |

|

|

|

|

|

43 |

Other expenses (itemize): (a) |

|

|

|

|

|

(b) |

|

|

|

|

|

(c) |

|

|

|

|

|

(d) |

|

|

|

|

|

(e) |

|

|

|

|

|

(f) |

|

|

|

|

44 |

Total functional expenses (add lines 22 through 43) |

|

|

|

|

PART III STATEMENT OF PROGRAM SERVICES RENDERED |

|

|

|

||

List each program service title on lines (a) through (d); for each, identify the service output(s) or Product(s) and report the quantity provided. Enter the total expenses attributable to each program service and the amount of grants and allocations included in that total.

(a)__________________________________________________________________________________________

__________________________________________________________________________________________

__________________________________________________________________________________________

__________________________________________________________________________________________

(Grants and allocations $ |

) |

(b)__________________________________________________________________________________________

__________________________________________________________________________________________

__________________________________________________________________________________________

__________________________________________________________________________________________

(Grants and allocations $ |

) |

(c)__________________________________________________________________________________________

__________________________________________________________________________________________

__________________________________________________________________________________________

__________________________________________________________________________________________

(Grants and allocations $ |

) |

(d)__________________________________________________________________________________________

__________________________________________________________________________________________

__________________________________________________________________________________________

__________________________________________________________________________________________

|

(Grants and allocations $ |

) |

(e) Other program service activities (attach schedule) |

(Grants and allocations $ |

) |

(f) Total (add lines (a) through (3)) (should equal line 44(B)) |

|

|

|

|

|

|

|

|

|

|

Page 3 |

|

PART IV PROGRAM SERVICE REVENUE AND OTHER REVENUE (STATE NATURE) |

|

Program |

|

Other |

|||||

|

|

|

|

|

|

service revenue |

|

revenue |

|

(a) Fees from government agencies |

. . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

. . . . . . . . . . . |

|

|

|

|

||

(b) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

. . . . . . . . . . . |

|

|

|

|

||

(c) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

. . . . . . . . . . . . |

|

|

|

|

|

(d) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

. . . . . . . . . . . . |

|

|

|

|

|

(e) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

. . . . . . . . . . . . |

|

|

|

|

|

(f) Total program service revenue (enter here and on line 2) |

. . . . . . . . . . . . . . |

. . . . . . . . . . . . |

|

|

|

|

|||

(g) Total other revenue (enter here and on line 11) |

. . . . . . . . . . . . . . |

. . . . . . . . . . . . |

|

|

|

|

|||

PART V BALANCE SHEETS |

If line 12, Part 1, and line 59 are $25,000 or less, you should complete only lines 59, 66, and 74 and, if you do not |

||||||||

Use fund accounting, line 73. If line 12 or line 59 is more than $25,000, complete the entire balance sheet. |

|||||||||

|

|

||||||||

Note: Columns (C) and (D) are optional. Columns (A) and (B) must be |

(A) Beginning of |

|

|

End of year |

|

|

|||

completed to the extent applicable. Where required, attach schedules should be |

(B) Total |

|

(C) Unrestricted/ |

|

(D) Restricted/ |

||||

year |

|

|

|||||||

for |

|

|

|

Expendable |

|

Nonexpendable |

|||

|

|

|

|

|

|||||

|

Assets |

|

|

|

|

|

|

|

|

45 |

Cash — |

|

|

|

|

|

|

||

46 |

Savings and temporary cash investments |

|

|

|

|

|

|

||

47 |

Accounts receivable _______ |

|

|

|

|

|

|

|

|

|

minus allowance for doubtful accounts ____________ |

|

|

|

|

|

|

||

48 |

Pledges receivable ________ |

|

|

|

|

|

|

|

|

|

minus allowance for doubtful accounts ____________ |

|

|

|

|

|

|

||

49 |

Grants receivable |

|

|

|

|

|

|

||

50 |

Receivable due from officers, directors, trustees and key |

|

|

|

|

|

|

||

|

employees (attach schedule) |

. . . . . . . . . . . . . . . . . |

|

|

|

|

|

|

|

51 |

Other notes and loans receivable ____________ |

|

|

|

|

|

|

||

|

minus allowance for doubtful accounts ____________ |

|

|

|

|

|

|

||

52 |

Inventories for sale or use |

. . . . . . . . . . . . . . . . . |

|

|

|

|

|

|

|

53 |

Prepaid expenses and deferred charges |

|

|

|

|

|

|

||

54 |

Investments — securities (attach schedule) |

|

|

|

|

|

|

||

55 |

Investments — land, buildings and equipment: basis ____ |

|

|

|

|

|

|

||

|

minus allowance for doubtful accounts ____________ |

|

|

|

|

|

|

||

56 |

Investments — other (attach schedule) |

|

|

|

|

|

|

||

57 |

Land, buildings and equipment: basis _________ |

|

|

|

|

|

|

||

|

minus accumulated depreciation ______ (attach schedule) |

|

|

|

|

|

|

||

58 |

Other assets _____________ |

|

|

|

|

|

|

|

|

59 |

Total assets (add lines 45 through 58) |

|

|

|

|

|

|

||

|

Liabilities |

|

|

|

|

|

|

|

|

60 |

Accounts payable and accrued expenses |

|

|

|

|

|

|

||

61 |

Grants payable |

|

|

|

|

|

|

||

62 |

Support and revenue designated for future periods |

|

|

|

|

|

|

||

|

(attach schedule) |

|

|

|

|

|

|

||

63 |

Loans from officers, directors, trustees, and key employees |

|

|

|

|

|

|

||

|

(attach schedule) |

. . . . . . . . . . . . . . . . . |

|

|

|

|

|

|

|

64 |

Mortgages and other notes payable (attach schedule) |

|

|

|

|

|

|

||

65 |

Other liabilities ___________ |

|

|

|

|

|

|

|

|

66 |

Total liabilities (add lines 60 through 65) |

|

|

|

|

|

|

||

|

Fund Balances or Net Worth |

|

|

|

|

|

|

||

Organizations that use fund accounting, check here |

|

|

|

|

|

|

|||

and complete lines 67 through 70 and lines 74 and 75. |

|

|

|

|

|

|

|||

67 a. Current unrestricted fund |

|

|

|

|

|

|

|||

|

b. Current restricted fund |

. . . . . . . . . . . . . . . . . . |

|

|

|

|

|

|

|

68 |

Land, buildings and equipment fund |

|

|

|

|

|

|

||

69 |

Endowment fund |

. . . . . . . . . . . . . . . . . |

|

|

|

|

|

|

|

70 |

Other funds (Describe _________ ) |

|

|

|

|

|

|

||

Organizations that do not use fund accounting, check here |

|

|

|

|

|

|

|||

and complete lines 71 through 75. |

|

|

|

|

|

|

|

||

71 |

Capital stock or trust principal |

|

|

|

|

|

|

||

72 |

|

|

|

|

|

|

|||

73 |

Retained earnings or accumulated income |

|

|

|

|

|

|

||

74 |

Total fund balances or new worth |

|

|

|

|

|

|

||

75 |

Total liabilities and fund balances/net worth |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

Page 4 |

|

|

PART VI LIST OF OFFICERS, DIRECTORS & TRUSTEES (LIST OFFICER, DIRECTOR & TRUSTEE WHETHER |

|||||||

|

COMPENSATED OR NOT) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NAME AND ADDRESS |

TITLE & AVERAGE |

COMPENSATION |

|

|

EMPLOYEE |

||

|

|

HOURS PER WEEK |

(if any) |

|

|

BENEFITS |

||

|

|

DEVOTED TO |

|

|

|

|

|

|

|

|

POSITION |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

PART VII COMPENSATION OF FIVE HIGHEST PAID PERSONS FOR PROFESSIONAL SERVICES |

|

|

|||||

|

|

|

|

|

|

|

||

|

NAME AND ADDRESS OF PERSONS PAID MORE THAN $30,000 |

|

TYPE OF SERVICE |

|

COMPENSATION |

|||

|

|

|

|

|

|

|

PAID |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL NUMBER OF OTHERS RECEIVING OVER $30,000 for professional services . . . . . . . . . . . . . . _____________________

76 Have any changes been made in the organizing or governing documents? Yes ____ No ____

If yes, attach a copy of the changes.

77 Is the organization related (other than by association with a statewide or nationwide organization) through common membership, governing bodies, trustees, officers, etc., to any other exempt or nonexempt organization? Yes ____ No ____

78 Did your organization receive donated services or the use of materials, equipment or facilities at no charge or at substantially less than fair rental value? Yes ____ No ____

79 The financial books are in the care of _________________________________________________________________________

Located at ______________________________________________________________________________________________

Telephone number ________________________________________________________________________________________

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

UNDER THE PENALTIES OF PERJURY, I DECLARE THAT I HAVE EXAMINED THIS REPORT, INCLUDING ACCOMPANYING STATEMENTS AND TO THE BEST OF MY KNOWLEDGE AND BELIEF IT IS TRUE, CORRECT AND COMPLETE.

Name of Officer __________________________________________________ Date ________________ Title ____________

Signature of Officer _____________________________________________________________________________________

Incomplete Organization Information: Many individuals forget to provide complete details about their organization, such as the name, address, and fiscal year ending date. This information is crucial for proper identification and processing.

Incorrect Financial Figures: Errors in reporting revenue, expenses, or changes in net assets can lead to significant issues. Double-checking all figures before submission can help avoid discrepancies that may require revisions later.

Missing Attachments: Certain sections of the form require additional schedules or explanations. Failing to attach these documents can delay processing and may result in penalties.

Failure to Sign and Date: A common oversight is neglecting to sign and date the form. This step is necessary to validate the submission and confirm that the information is accurate to the best of the officer's knowledge.

Neglecting to Review Changes: Organizations that have made changes in their governing documents must attach a copy of these changes. Not doing so can lead to confusion and potential compliance issues.

What is the Maryland Cof 85 form?

The Maryland Cof 85 form is a financial reporting document required for organizations that are not filing Form 990. It helps the state gather information about the organization's revenue, expenses, and overall financial health for a specific fiscal year. This form is essential for maintaining transparency and compliance with state regulations.

Who needs to file the Maryland Cof 85 form?

Organizations that are exempt from federal income tax under Section 501(c)(3) and do not meet the criteria for filing Form 990 must complete the Maryland Cof 85 form. This typically includes smaller nonprofits and charitable organizations that have total revenue of less than $200,000 and total assets of less than $500,000.

What information is required on the Maryland Cof 85 form?

The form requires detailed information about the organization's financial activities. This includes contributions received, program service revenue, membership dues, expenses, and changes in net assets. Organizations must also provide a breakdown of functional expenses, program services rendered, and a balance sheet detailing assets and liabilities.

When is the Maryland Cof 85 form due?

The Maryland Cof 85 form is typically due on the 15th day of the 5th month after the end of the organization's fiscal year. For organizations that operate on a calendar year, this means the form is due on May 15. It’s important to check for any specific deadlines or extensions that may apply.

How do I submit the Maryland Cof 85 form?

The form can be submitted either by mail or electronically, depending on the preferences of the organization and the requirements set by the Maryland Secretary of State. If mailing, ensure that the form is sent to the correct address, which is usually the Secretary of State's office in Annapolis, Maryland.

What happens if I miss the deadline for filing the Maryland Cof 85 form?

Missing the deadline can lead to penalties and potential loss of tax-exempt status. Organizations may face late fees, and repeated failures to file can result in administrative dissolution. It's crucial to file on time or seek an extension if necessary.

Can I amend the Maryland Cof 85 form after submission?

Yes, if you discover an error after submitting the form, you can file an amendment. It's important to provide a clear explanation of the changes made. Contact the Maryland Secretary of State’s office for specific instructions on how to proceed with an amendment.

Where can I find assistance with completing the Maryland Cof 85 form?

Assistance can be found through various resources, including nonprofit support organizations, accountants familiar with nonprofit tax law, and the Maryland Secretary of State’s office. Many organizations also offer workshops or guides to help with the completion of the form.