Fill Out Your Maryland 510E Template

Fill Out Your Maryland 510E Template

When filling out the Maryland 510E form, it is important to follow certain guidelines to ensure the application is processed smoothly. Below is a list of things to do and avoid.

By adhering to these guidelines, the chances of a successful application for an extension of time to file the pass-through entity income tax return will increase significantly.

Misconception 1: The Maryland 510E form automatically extends the time to pay taxes.

Many people believe that filing the 510E form gives them extra time to pay their taxes. This is not true. The form only extends the time to file the return, not the time to pay any taxes owed. Payment is still due by the original deadline.

Misconception 2: You can file the 510E form anytime before the tax deadline.

Some think they can submit the 510E form at their convenience. In reality, it must be filed by the original due date of the tax return. For S corporations, that’s the 15th day of the 3rd month after the tax year ends. For partnerships and LLCs, it’s the 15th day of the 4th month.

Misconception 3: You don’t need to file an extension with the IRS to use the 510E form.

This is a common misunderstanding. To qualify for an extension in Maryland, you must also file an extension with the IRS or provide a valid reason for not doing so. Failing to do this can lead to your extension being denied.

Misconception 4: The 510E form can be used for any type of tax entity.

Not all entities can use the 510E form. It is specifically for pass-through entities like partnerships, S corporations, and limited liability companies. Other business structures have different requirements.

Misconception 5: You can receive multiple extensions by filing the 510E form multiple times.

This is incorrect. Maryland law allows only one automatic extension of up to six months. If you need more time beyond that, you must provide a valid reason and file an additional request.

Maryland Tax Filing Requirements - Fees related to the recording charges and state taxes are outlined for transparency.

When parents decide to educate their children at home, one crucial step is to complete the Virginia Homeschool Letter of Intent, which can be found at homeschoolintent.com/editable-virginia-homeschool-letter-of-intent/. This document not only informs the local school division of their decision but also signifies a commitment to providing a comprehensive educational experience away from conventional schooling.

Maryland Intake Sheet - The Maryland Intake Sheet is essential for recording land instruments efficiently.

Filling out the Maryland 510E form can seem daunting, but understanding its key components can simplify the process. Here are some essential takeaways to keep in mind:

By keeping these points in mind, you can navigate the Maryland 510E form with greater ease and confidence. Proper preparation and attention to detail will help ensure a smoother process.

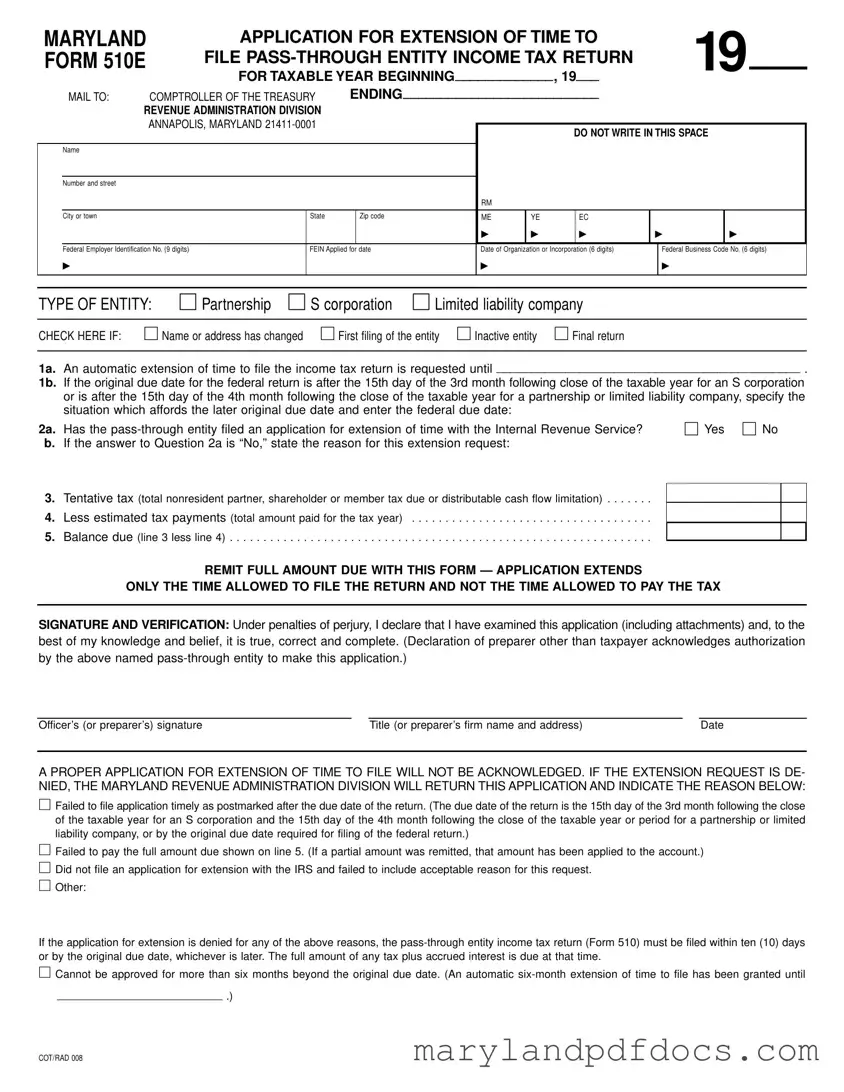

Filling out the Maryland 510E form requires careful attention to detail. This form is essential for requesting an extension of time to file a pass-through entity income tax return. Completing it accurately ensures that the request is processed smoothly and that any necessary payments are made on time.

MARYLAND |

APPLICATION FOR EXTENSION OF TIME TO |

|

|

19 |

|

|||||||||||

FORM 510E |

FILE |

|

|

|

||||||||||||

|

|

FOR TAXABLE YEAR BEGINNING_____________, 19___ |

|

|

|

|||||||||||

|

MAIL TO: |

COMPTROLLER OF THE TREASURY |

ENDING__________________________ |

|

|

|

|

|

||||||||

|

REVENUE ADMINISTRATION DIVISION |

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

ANNAPOLIS, MARYLAND |

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

DO NOT WRITE IN THIS SPACE |

|||||||||

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Number and street |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

RM |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City or town |

|

|

State |

|

Zip code |

|

ME |

YE |

|

EC |

|

|

|

|

|

|

|

|

|

|

|

|

|

▶ |

▶ |

|

▶ |

▶ |

|

▶ |

||

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Federal Employer Identification No. (9 digits) |

|

FEIN Applied for date |

|

Date of Organization or Incorporation (6 digits) |

|

Federal Business Code No. (6 digits) |

|||||||||

|

▶ |

|

|

|

|

|

|

▶ |

|

|

|

|

▶ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|||||||||

TYPE OF ENTITY: ☐ Partnership |

☐ S corporation |

☐ Limited liability company |

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

||||||||||

CHECK HERE IF: ☐ Name or address has changed ☐ First filing of the entity ☐ Inactive entity |

☐ Final return |

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1a. |

An automatic extension of time to file the income tax return is requested until ____________________________________________ . |

|

1b. |

If the original due date for the federal return is after the 15th day of the 3rd month following close of the taxable year for an S corporation |

|

|

or is after the 15th day of the 4th month following the close of the taxable year for a partnership or limited liability company, specify the |

|

|

situation which affords the later original due date and enter the federal due date: |

|

2a. |

Has the |

☐ Yes ☐ No |

b.If the answer to Question 2a is “No,” state the reason for this extension request:

3.Tentative tax (total nonresident partner, shareholder or member tax due or distributable cash flow limitation) . . . . . . .

4.Less estimated tax payments (total amount paid for the tax year) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

5. Balance due (line 3 less line 4) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

REMIT FULL AMOUNT DUE WITH THIS FORM — APPLICATION EXTENDS

ONLY THE TIME ALLOWED TO FILE THE RETURN AND NOT THE TIME ALLOWED TO PAY THE TAX

SIGNATURE AND VERIFICATION: Under penalties of perjury, I declare that I have examined this application (including attachments) and, to the best of my knowledge and belief, it is true, correct and complete. (Declaration of preparer other than taxpayer acknowledges authorization by the above named

Officer’s (or preparer’s) signature |

Title (or preparer’s firm name and address) |

Date |

A PROPER APPLICATION FOR EXTENSION OF TIME TO FILE WILL NOT BE ACKNOWLEDGED. IF THE EXTENSION REQUEST IS DE- NIED, THE MARYLAND REVENUE ADMINISTRATION DIVISION WILL RETURN THIS APPLICATION AND INDICATE THE REASON BELOW:

☐Failed to file application timely as postmarked after the due date of the return. (The due date of the return is the 15th day of the 3rd month following the close of the taxable year for an S corporation and the 15th day of the 4th month following the close of the taxable year or period for a partnership or limited liability company, or by the original due date required for filing of the federal return.)

☐Failed to pay the full amount due shown on line 5. (If a partial amount was remitted, that amount has been applied to the account.)

☐Did not file an application for extension with the IRS and failed to include acceptable reason for this request.

☐Other:

If the application for extension is denied for any of the above reasons, the

☐Cannot be approved for more than six months beyond the original due date. (An automatic

___________________________ .)

COT/RAD 008

INSTRUCTIONS FOR MARYLAND FORM 510E (Revised 1999)

APPLICATION FOR EXTENSION OF TIME

TO FILE

INCOME TAX RETURN

GENERAL INSTRUCTIONS

Purpose of Form Form 510E is used by a

General Requirements Maryland law provides for an extension of time to file, but in no case can an extension be granted for more than six months beyond the original due date. A request for exten- sion of time to file will be granted auto- matically for six months for S corporations and three months for partnerships and limited liability companies if:

1)Form 510E is properly filed and submitted by the original due date (S corporation: 15th day of the 3rd month following close of the tax year or period. Partnerships and limited liability companies: 15th day of the 4th month following close of the tax year or period.);

2)full payment of any balance due is submitted with Form 510E; and

3)an application for extension of time has been filed with the Internal Revenue Service or an acceptable reason has been provided with Form 510E.

An additional

A proper application for extension of time to file will not be acknowledged. If the extension request is denied, the

Form 510E does not extend the time allowed a

When and Where to File File Form 510E by the 15th day of the 3rd month following the close of the taxable year or period if an S corporation; by the 15th day of the 4th month following the close of the taxable year or period if a partnership or limited liability company. The return must be filed with the Comptroller of the Treasury, Revenue Administration Division, Annapolis, Maryland

SPECIFIC INSTRUCTIONS

Taxable Year or Period Enter the beginning and ending dates of the tax- able year in the space provided at the top of Form 510E.

Name, Address and Other Information

Type or print the required information in the designated area. DO NOT USE THE LABEL FROM THE TAX BOOKLET COVER.

Enter the exact

Enter the Federal Employer Identifica- tion Number (FEIN). If a FEIN has not been secured, enter “APPLIED FOR” followed by the date of application. If a FEIN has not been applied for, do so immediately.

Be sure to check the applicable box to indicate the type of

Check the applicable box if: (1) the name or address has changed; (2) this is the first filing of the

(3)this is an inactive

Tentative Tax Enter the total amount of income tax liability expected for the tax year on line 3.

Estimated Tax Payments Enter on line 4 the total amounts paid with Form 510D - Declaration of Estimated Pass- Through Entity Nonresident Tax for the taxable year or period.

Balance Due Enter the amount of tax due on line 5 and remit full payment with this form.

Signature and Verification An author- ized officer or the paid preparer must sign and date Form 510E indicating the officer’s title or preparer firm name and address.

Payment Instructions Include a check or money order made payable to the Comptroller of the Treasury for the full amount of any balance due. All payments must indicate the Federal Employer Identi- fication Number, type of tax and tax year beginning and ending dates. DO NOT SEND CASH.

Mailing Instructions Use the enve- lope provided in the tax booklet and place an “X” in the appropriate box in the lower left corner to indicate the type of document enclosed. Also, be sure to read and follow the reminders listed on the back of the envelope.

Failing to Submit by the Deadline: One common mistake is not filing the Maryland 510E form by the required deadline. For S corporations, this is the 15th day of the 3rd month after the close of the taxable year. For partnerships and limited liability companies, it is the 15th day of the 4th month. Missing this deadline can result in the denial of the extension request.

Omitting the Federal Employer Identification Number (FEIN): Applicants often forget to include their FEIN. This number is essential for identifying the entity and must be provided accurately. If a FEIN has not been secured, the applicant should write “APPLIED FOR” along with the date of application.

Not Paying the Full Amount Due: Another frequent error involves failing to remit the full balance due when submitting the form. The application for extension does not extend the time allowed to pay taxes. Therefore, any balance must be paid in full at the time of filing to avoid penalties.

Incorrectly Indicating the Type of Entity: Many individuals mistakenly check the wrong box for the type of entity. It is crucial to accurately identify whether the entity is a partnership, S corporation, or limited liability company. This information affects the filing requirements and deadlines.

What is the Maryland 510E form?

The Maryland 510E form is an application used by pass-through entities, such as partnerships, S corporations, and limited liability companies, to request an extension of time to file their income tax return. This form allows entities to extend their filing deadline, but it does not extend the time to pay any taxes owed.

Who needs to file the Maryland 510E form?

If you are operating a pass-through entity in Maryland and require additional time to prepare your income tax return, you will need to file the Maryland 510E form. This includes partnerships, S corporations, and limited liability companies that may not be able to meet the original filing deadline.

When is the Maryland 510E form due?

The due date for filing the Maryland 510E form depends on the type of entity. For S corporations, the form must be submitted by the 15th day of the 3rd month following the close of the taxable year. For partnerships and limited liability companies, the due date is the 15th day of the 4th month following the close of the taxable year.

What happens if my extension request is denied?

If the Maryland Revenue Administration Division denies your extension request, you will be notified. In such cases, you must file the pass-through entity income tax return (Form 510) within ten days of the denial or by the original due date, whichever is later. Be aware that any unpaid taxes will incur interest and penalties.

Do I need to pay taxes when I file the Maryland 510E form?

Yes, when submitting the Maryland 510E form, you must remit the full amount of any taxes due. The extension only grants additional time to file your return, not to pay any taxes owed. Failure to pay the required amount may result in penalties and interest.

Can I get an additional extension beyond six months?

Generally, the Maryland 510E form allows for a maximum extension of six months. However, partnerships and limited liability companies may request an additional three-month extension for reasonable cause by submitting another Form 510E. This request must be justified with an acceptable reason.

What information do I need to provide on the Maryland 510E form?

You will need to provide several pieces of information, including the name and address of the pass-through entity, the Federal Employer Identification Number (FEIN), and the taxable year dates. Additionally, you must indicate the type of entity, any changes to the name or address, and the tentative tax amount expected for the year. Proper completion of the form is essential for the extension request to be acknowledged.