Fill Out Your Maryland 510D Template

Fill Out Your Maryland 510D Template

When filling out the Maryland 510D form, it is essential to follow specific guidelines to ensure accuracy and compliance. Below is a list of things you should and shouldn't do.

Misconception 1: The Maryland 510D form is only for S corporations.

Many people believe that the 510D form is exclusively for S corporations. In reality, this form is applicable to various pass-through entities (PTEs), including partnerships, limited liability companies (LLCs), and business trusts. Each of these entities can use the form to declare and remit estimated taxes on behalf of their nonresident members.

Misconception 2: The estimated tax payments are optional.

Some individuals think that making estimated tax payments is optional for pass-through entities. However, if the expected tax liability exceeds $1,000 for the tax year, these entities are required to make quarterly estimated payments. Failing to do so may result in interest and penalties, which can add financial strain.

Misconception 3: Nonresident members do not need to report taxes paid on their behalf.

Another common misconception is that nonresident members do not need to report the taxes paid on their behalf. In fact, the PTE must issue a statement to each nonresident member detailing the amount of tax paid. Nonresident members must include this statement with their own income tax returns to claim credit for the taxes paid on their behalf.

Misconception 4: The tax rates and rules are fixed and do not change.

Many assume that the tax rates and rules associated with the Maryland 510D form remain constant. However, the Maryland Legislature can change these rates during its sessions. It is essential for PTEs to stay informed about any updates by regularly checking the Maryland tax website for the most current information.

Dpss Verification Documents - Completing all questions on the application is crucial to avoid delays in processing.

To effectively navigate the refund process for overpaid taxes in Ohio, individuals and school districts can utilize the Ohio IT AR form, which is specifically designed for this purpose. Detailed instructions and resources can be found at Ohio PDF Forms, ensuring taxpayers complete the application correctly after filing their income tax returns.

Unemployment Beacon - Employers should verify that their payment options are correctly set up to avoid issues.

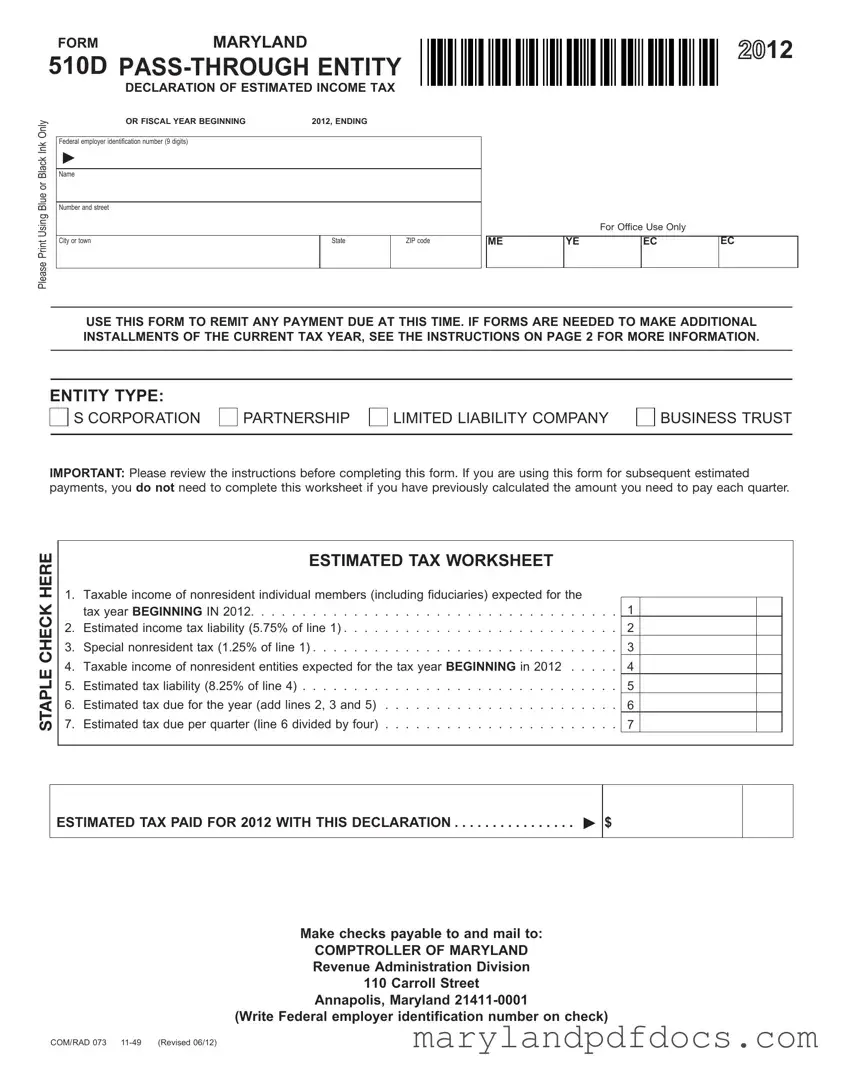

1. Purpose of the Form: The Maryland 510D form is used by pass-through entities (PTEs) to declare and remit estimated income tax on behalf of nonresident members.

2. Tax Rates: Nonresident individual members are taxed at 5.75%, while nonresident entity members face a tax rate of 8.25% on their distributive shares of income.

3. Estimated Payments: If the expected tax exceeds $1,000 for the year, PTEs must make quarterly estimated payments to avoid penalties. Payments should total at least 90% of the current year’s tax or 110% of the prior year’s tax.

4. Filing Deadlines: Form 510D must be filed on or before the 15th day of the 4th, 6th, 9th, and 12th months for S corporations, or by the 4th, 6th, 9th, and 13th months for partnerships, LLCs, and business trusts.

5. Required Information: The form requires the exact name of the PTE, the federal employer identification number (FEIN), and the tax year dates. If a FEIN is not yet secured, indicate “APPLIED FOR” and the application date.

6. Payment Instructions: Payments must be made via check or money order, payable to the Comptroller of Maryland. Include the FEIN and tax year details on the payment. Do not send cash.

Completing the Maryland 510D form is a necessary step for pass-through entities to declare and remit estimated income tax. After you fill out the form, you will need to submit it along with your payment to the appropriate state authority. Below are the steps to guide you through the process of filling out the Maryland 510D form.

FORMMARYLAND

510D

DECLARATION OF ESTIMATED INCOME TAX

Only |

OR FISCAL YEAR BEGINNING |

2012, ENDING |

|

|

|

|

|

|

|

Ink |

Federal employer identification number (9 digits) |

|

|

|

|

|

|

|

|

Black |

|

|

|

|

Name |

|

|

|

|

or |

|

|

|

|

Blue |

|

|

|

|

Number and street |

|

|

|

|

Using |

|

|

|

|

City or town |

|

State |

ZIP code |

|

|

|

|

|

|

Please |

|

|

|

|

|

|

|

|

|

ME

12

12

For Office Use Only

YE |

EC |

EC |

|

|

|

USE THIS FORM TO REMIT ANY PAYMENT DUE AT THIS TIME . IF FORMS ARE NEEDED TO MAKE ADDITIONAL INSTALLMENTS OF THE CURRENT TAX YEAR, SEE THE INSTRUCTIONS ON PAGE 2 FOR MORE INFORMATION .

ENTITY TYPE:

S CORPORATION

PARTNERSHIP

LIMITED LIABILITY COMPANY

BUSINESS TRUST

IMPORTANT: Please review the instructions before completing this form. If you are using this form for subsequent estimated payments, you do not need to complete this worksheet if you have previously calculated the amount you need to pay each quarter.

STAPLE CHECK HERE

ESTIMATED TAX WORKSHEET

1.Taxable income of nonresident individual members (including fiduciaries) expected for the

tax year BEGINNING IN 2012. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1. . BEGINNING in 2011

2.Estimated income tax liability (5.75% of line 1) . . . . . . . . . . . . . . . . . . . . . . . . . . . .2. .

3.Special nonresident tax (1.25% of line 1) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3. .

4.Taxable income of nonresident entities expected for the tax year BEGINNING in 2012 . . . . . .4. .

5.Estimated tax liability (8.25% of line 4) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .5. .

6.Estimated tax due for the year (add lines 2, 3 and 5) . . . . . . . . . . . . . . . . . . . . . . . .6. .

7.Estimated tax due per quarter (line 6 divided by four) . . . . . . . . . . . . . . . . . . . . . . . .7. .

ESTIMATED TAX PAID FOR 2012 WITH THIS DECLARATION |

$ |

|

|

|

|

Make checks payable to and mail to:

COMPTROLLER OF MARYLAND Revenue Administration Division 110 Carroll Street

Annapolis, Maryland

(Write Federal employer identification number on check)

COM/RAD 073

INSTRUCTIONS MARYLAND

FOR |

DECLARATION OF ESTIMATED INCOME TAX |

|

FORM 510D |

||

|

||

2012 |

|

Purpose of Form Form 510D is used by a pass- through entity (PTE) to declare and remit estimated tax.

General Requirements PTEs are required to pay tax on behalf of all nonresident members. For nonresident members that are individuals or nonresident fiduciaries, the tax is 5.75% in addition to the special nonresident tax of 1.25% of the nonresident member’s distributive or pro rata share of income. For nonresident entity members, the tax is 8.25% of the nonresident member’s distributive or pro rata share of income. A nonresident entity is an entity that is not formed under the laws of Maryland; and is not qualified by, or registered with the Department of Assessments and Taxation to do business in Maryland. The amount of tax due may be limited based on the distributable cash flow limitation. The Distributable Cash Flow Limitation worksheet is available in our PTE income tax booklet, which can be downloaded at www . marylandtaxes .com.

Certain PTEs meeting certain reporting requirements are exempt from the requirement to pay nonresident tax on behalf of its nonresident members. See instructions for Form 510 for more information.

When the tax is expected to exceed $1,000 for the tax year, the PTE must make quarterly estimated payments. The total estimated tax payments for the year must be at least 90% of the tax developed for the current tax year or 110% of the tax that was developed for the prior tax year to avoid interest and penalty.

In the case of a short tax period the total estimated tax required is the same as for a regular tax year: 90% of the tax that was developed for the current (short) tax year or 110% of the tax that was developed for the prior tax year. The minimum estimated tax for each of the installment due dates is the total estimated tax required divided by the number of installment due dates occurring during the short tax year. However, if the

Maryland law provides for the accrual of interest and imposition of penalty for failure to pay any tax when due.

If it is necessary to amend the estimate, recalculate the amount of estimated tax required using the estimated tax worksheet provided. Adjust the amount of the next installment to reflect any previous underpayment or overpayment. The remaining installments must be at least 25% of the amended estimated tax due for the year.

The PTE must issue a statement to each nonresident member showing the amount of tax paid on their behalf. Nonresident members must include the statement with their own income tax returns (Form 500, 504, 505 or 510) to claim credit for taxes paid on their behalf.

Tax Rate The current 2012 tax rate for nonresident individual members is 5.75% at the time this form was created. It is possible that the Maryland Legislature may change this tax when in session. Please check our Web site for updates at www .marylandtaxes .com.

When to File File Form 510D on or before the 15th day of the 4th, 6th, 9th and 12th months following the beginning of the tax year or period for S corporations or by the 4th, 6th, 9th and 13th months following the beginning of the tax year for partnerships, LLCs and business trusts.

Tax Year or Period The tax year is shown at the top of Form 510D. The form used for filing must reflect the preprinted tax year in which the PTE’s tax year begins.

If the tax year of the PTE is other than a calendar year, enter the beginning and ending dates of the fiscal year in the space provided at the top of Form 510D.

Name, Address, and Other Information Type or print the required information in the designated area.

Enter the exact PTE name with any “Trading As” (T/A) name if applicable.

Enter the federal employer identification number (FEIN). If the FEIN has not been secured, enter “APPLIED FOR” followed by the date of application. If a FEIN has not been applied for, do so immediately.

Filing electronically using Modernized Electronic Filing method (software provider must be approved by the IRS and Revenue Administration Division). If filed electronically, do not mail 510D; retain it with company’s records .

If you need to make additional payments for the current tax year you may file electronically, or you can go to

www.marylandtaxes .comand download another Form 510D. We have discontinued the use of preprinted quarterly estimated tax vouchers for PTEs.

Payment Instructions Include a check or money order made payable to Comptroller of Maryland. All payments must indicate the FEIN, type of tax and tax year beginning and ending dates. DO NOT SEND CASH.

Mailing Instructions Mail the completed Form 510D and payment to:

Comptroller of Maryland

Revenue Administration Division

110 Carroll Street

Annapolis, MD

COM/RAD 073

Incorrect Entity Type Selection: Many individuals fail to select the correct entity type, such as S Corporation, Partnership, Limited Liability Company, or Business Trust. This selection affects tax rates and obligations.

Missing Federal Employer Identification Number (FEIN): Some filers neglect to include their FEIN. This number is crucial for identification and processing, so it should always be provided.

Improper Calculation of Estimated Tax: Errors in calculating the estimated tax liability can lead to underpayment or overpayment. It is essential to use the provided worksheet accurately.

Failure to Sign and Date the Form: Not signing or dating the form is a common oversight. A signature is required for the form to be valid.

Incorrect Payment Amount: Individuals sometimes send the wrong payment amount, either due to miscalculations or misunderstanding of the payment instructions.

Neglecting to Include Payment Information: Some filers forget to indicate the type of tax and the tax year on their payment. This can lead to delays in processing.

Using an Outdated Form: Utilizing an outdated version of Form 510D can result in incorrect filing. Always ensure that you are using the most current form available.

Improper Mailing: Sending the form and payment to the wrong address can cause significant delays. Ensure that you mail it to the correct address provided in the instructions.

Ignoring Filing Deadlines: Failing to file by the specified deadlines can lead to penalties and interest. It is crucial to be aware of and adhere to these deadlines.

What is the purpose of the Maryland 510D form?

The Maryland 510D form is designed for pass-through entities (PTEs) to declare and remit estimated income tax. This form is particularly important for PTEs that have nonresident members, as it ensures that the appropriate taxes are paid on their behalf. By using this form, PTEs can calculate their estimated tax liabilities and make necessary payments to avoid penalties.

Who needs to file the Maryland 510D form?

Any pass-through entity, such as an S corporation, partnership, limited liability company, or business trust, with nonresident members is required to file the Maryland 510D form. If the PTE expects to owe more than $1,000 in taxes for the year, it must make quarterly estimated payments. This requirement helps ensure that nonresident members are properly taxed on their share of the entity's income.

How is the estimated tax calculated on the Maryland 510D form?

To calculate the estimated tax, the PTE first determines the taxable income of its nonresident members. For individual members, the tax rate is 5.75%, plus a special nonresident tax of 1.25%. For nonresident entities, the tax rate is 8.25%. The total estimated tax due for the year is the sum of these calculations, which is then divided by four to find the quarterly estimated tax payment.

When are the payments due for the Maryland 510D form?

Payments for the Maryland 510D form are due on specific dates. For S corporations, the payments must be made by the 15th day of the 4th, 6th, 9th, and 12th months following the start of the tax year. For partnerships, LLCs, and business trusts, the due dates are the 4th, 6th, 9th, and 13th months. It’s crucial to meet these deadlines to avoid interest and penalties.

What happens if the estimated tax needs to be amended?

If a PTE realizes that its estimated tax needs to be adjusted, it can recalculate the required amount using the estimated tax worksheet provided with the form. Any adjustments should be reflected in the next installment payment. It's important to ensure that the remaining installments are at least 25% of the amended estimated tax due for the year to stay compliant.

How should payments be submitted with the Maryland 510D form?

When submitting the Maryland 510D form, include a check or money order made payable to the Comptroller of Maryland. Be sure to write the federal employer identification number (FEIN) on the payment, along with the type of tax and the tax year dates. Payments should be mailed to the Comptroller of Maryland's Revenue Administration Division in Annapolis. Remember, cash should never be sent.