Fill Out Your Maryland 504 Template

Fill Out Your Maryland 504 Template

When it comes to filling out the Maryland 504 form, there are several important dos and don'ts to keep in mind. Following these guidelines can help ensure that your submission is accurate and complete.

Unclaimed Property Maryland Claim Form - Add the date of your signature to ensure your claim is processed in a timely manner.

To ensure the protection of sensitive business information, it is important to understand the implications of a thorough Non-disclosure Agreement form. This agreement forms a crucial part of negotiations and collaborations, safeguarding the interests of all parties involved.

Daycare for Single Moms - It is important to state the number of college or technical school students within the household.

Maryland Dc 70 - Failure to provide adequate reasons may lead to denial of the request.

When dealing with the Maryland 504 form, there are several important points to keep in mind to ensure accurate and efficient filing. Here are key takeaways:

Filing the Maryland 504 form accurately is crucial for compliance and to avoid potential penalties. Taking the time to understand each section will facilitate a smoother process.

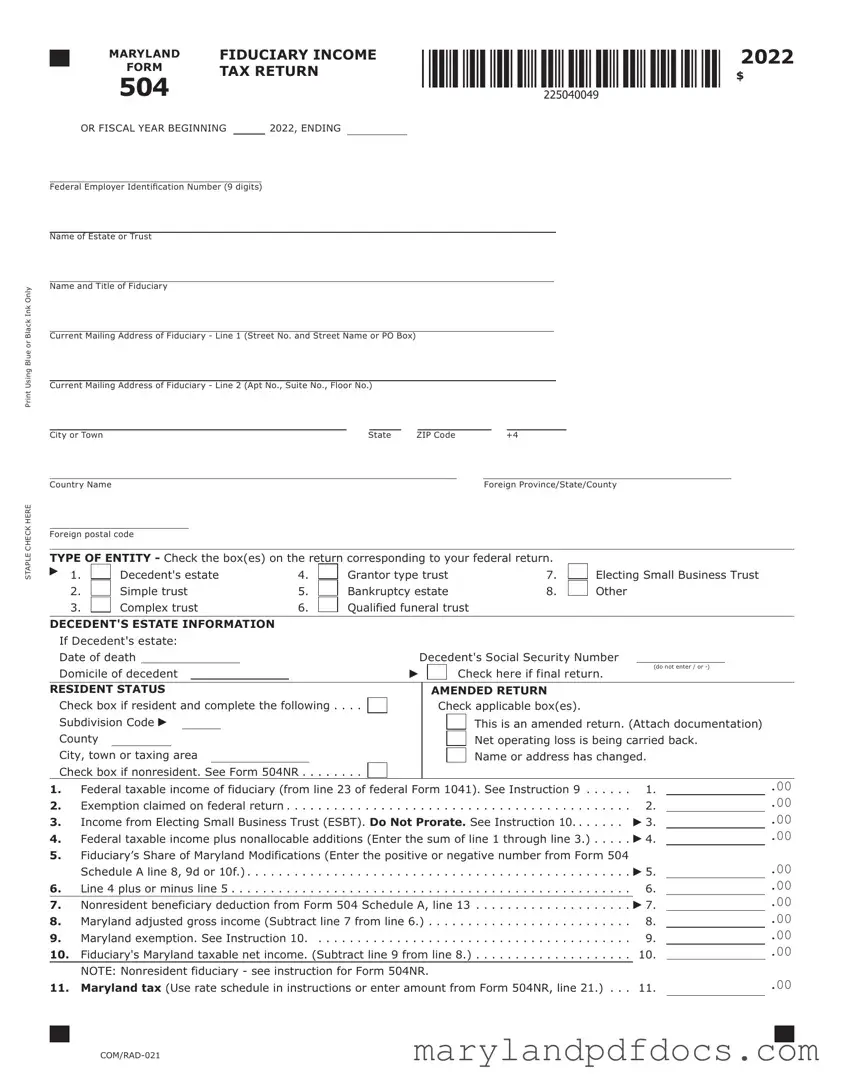

Filling out the Maryland 504 form requires careful attention to detail. This form is essential for reporting fiduciary income tax for estates and trusts. Before beginning, ensure you have all necessary information and documentation at hand, including the federal employer identification number, details about the estate or trust, and any relevant financial information. The following steps outline the process for completing the Maryland 504 form accurately.

|

|

MARYLAND |

FIDUCIARY INCOME |

|

|||||

|

|

|

|||||||

|

|

FORM |

TAX RETURN |

|

|||||

|

|

|

|||||||

|

504 |

|

|

|

|

|

|

|

|

|

|

OR FISCAL YEAR BEGINNING |

2022, ENDING |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

Federal Employer Identification Number (9 digits) |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

Name of Estate or Trust |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Black Ink Only |

Name and Title of Fiduciary |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Current Mailing Address of Fiduciary - Line 1 (Street No. and Street Name or PO Box) |

|

||||||||

Using Blue or |

|

|

|

|

|

||||

Current Mailing Address of Fiduciary - Line 2 (Apt No., Suite No., Floor No.) |

|

||||||||

|

|

|

|

|

|

|

|

|

|

2022

$

STAPLE CHECK HERE

|

City or Town |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

State |

|

ZIP Code |

|

|

|

+4 |

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

Country Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Foreign Province/State/County |

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

Foreign postal code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

TYPE OF ENTITY - Check the box(es) on the return corresponding to your federal return. |

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||

|

|

1. |

|

Decedent's estate |

4. |

|

|

|

|

Grantor type trust |

7. |

|

|

|

Electing Small Business Trust |

|

|

|

||||||||||||||||||||||||

|

|

2. |

|

Simple trust |

5. |

|

|

|

|

Bankruptcy estate |

8. |

|

|

|

Other |

|

|

|

|

|

|

|

||||||||||||||||||||

|

|

3. |

|

Complex trust |

6. |

|

|

|

|

Qualified funeral trust |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

DECEDENT'S ESTATE INFORMATION |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

If Decedent's estate: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

Date of death |

|

|

|

|

|

|

|

|

|

|

|

Decedent's Social Security Number |

|

|

|

|

|

|

|

||||||||||||||||||||||

|

Domicile of decedent |

|

|

|

|

|

|

|

|

|

|

|

|

|

Check here if final return. |

(do not enter / or |

|

|

|

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

RESIDENT STATUS |

|

|

|

|

|

|

|

|

|

|

|

AMENDED RETURN |

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

Check box if resident and complete the following |

|

|

|

|

|

Check applicable box(es). |

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

|

Subdivision Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

This is an amended return. (Attach documentation) |

|

|

|

||||||||||||||||||||||

|

County |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net operating loss is being carried back. |

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

City, town or taxing area |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name or address has changed. |

|

|

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||

|

Check box if nonresident. See Form 504NR |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

1. |

Federal taxable income of fiduciary (from line 23 of federal Form 1041). See Instruction 9 |

1. |

|

|

|

.00 |

|

|||||||||||||||||||||||||||||||||||

2. |

Exemption claimed on federal return |

2. |

|

|

|

.00 |

|

|||||||||||||||||||||||||||||||||||

3. |

.. .Income from Electing Small Business Trust (ESBT). Do Not Prorate. See Instruction 10 |

3. |

|

|

|

.00 |

|

|||||||||||||||||||||||||||||||||||

4. |

Federal taxable income plus nonallocable additions (Enter the sum of line 1 through line 3.) |

.. . . . . |

4. |

|

|

|

.00 |

|

||||||||||||||||||||||||||||||||||

5. |

Fiduciary’s Share of Maryland Modifications (Enter the positive or negative number from Form 504 |

|

|

|

|

.00 |

|

|||||||||||||||||||||||||||||||||||

|

|

Schedule A line 8, 9d or 10f.) |

. . . . . . . . . |

|

. . . 對 |

5. |

|

|

|

|

||||||||||||||||||||||||||||||||

6. |

Line 4 plus or minus line 5 |

6. |

|

|

|

.00 |

|

|||||||||||||||||||||||||||||||||||

7. |

Nonresident beneficiary deduction from Form 504 Schedule A, line 13 |

|

|

|

|

|

|

|

|

7. |

|

|

|

.00 |

|

|||||||||||||||||||||||||||

.. |

. |

. . |

. . . . . . . . |

. . . |

|

. . . . . |

|

|

|

|

||||||||||||||||||||||||||||||||

8. |

.. . . . . . . .Maryland adjusted gross income (Subtract line 7 from line 6.) |

. . |

. . . . . . . . |

. . . |

|

. . . . . |

8. |

|

|

|

.00 |

|

||||||||||||||||||||||||||||||

9. |

. .. . .Maryland exemption. See Instruction 10 |

. |

. . . |

. . |

. . |

. . |

. |

|

. . . |

. |

. |

. . |

. |

. . |

. . . . . . . . |

. . . |

|

. . . . . |

9. |

|

|

|

.00 |

|

||||||||||||||||||

10. |

Fiduciary's Maryland taxable net income. (Subtract line 9 from line 8.) |

.. |

. |

. . |

. . . . . . . . |

. . . |

|

. . . . . |

10. |

|

|

|

|

.00 |

|

|||||||||||||||||||||||||||

|

|

NOTE: Nonresident fiduciary - see instruction for Form 504NR. |

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|||||||||||||||||||||||||

11. |

Maryland tax (Use rate schedule in instructions or enter amount from Form 504NR, line 21.) .. . . |

11. |

|

|

|

|

||||||||||||||||||||||||||||||||||||

|

|

MARYLAND |

FIDUCIARY INCOME |

2022 |

||

|

|

|

|

|

|

|

|

|

FORM |

TAX RETURN |

page 2 |

||

|

||||||

504 |

|

|

|

|

||

NAME |

|

|

FEIN |

|

|

|

12.Special nonresident tax Nonresidents: Enter the amount from Form 504NR, line 22.

(See Instruction 14.) Residents: Enter zero. .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12.

13. Total Maryland tax (Add lines 11 and 12.).. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13.

14.Credit for fiduciary income tax paid to another state and/or credit for preservation and conservation

easements from Part AA, line 1 and Part AA, line 6 of Form 502CR (Attach Form 502CR.).. . . . 14.

15. Enter the Nonrefundable Business Tax Credits from Part AAA of Form 504CR. . . . . . . . . . . . . . .  15.

15.

16. Total credits (Add lines 14 and 15).. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16.

17. Maryland Tax after credits (Subtract line 16 from line 13, if less than zero, enter zero)... . . . . . . 17.

18.Local tax (Multiply the fiduciary's Maryland taxable net income from line 10 by

19. |

.0 |

|

). See Instruction 15. |

. . . |

. . . . . . . . . . . |

18. |

|

|

|

|

|||||

Local Credit for fiduciary income tax paid to another state from Part BB of Form 502CR |

19. |

||||||

20. |

Local tax after credit. (Subtract line 19 from line 18.) If less than zero, enter zero |

20. |

|||||

21. |

Total Maryland and local tax. (Add lines 17 and 20.) |

. . . |

. . . . . . . . . . . |

21. |

|||

22. |

Contribution to Chesapeake Bay and Endangered Species Fund |

22. |

|

|

.00 |

||

23. |

. . . .Contribution to Developmental Disabilities Services and Support Fund |

23. |

|

|

.00 |

||

24. |

Contribution to Maryland Cancer Fund |

24. |

|

|

.00 |

||

25. |

.. . . . . . . . . . . . . . . . . . . .Contribution to Fair Campaign Financing Fund |

25. |

|

|

.00 |

||

26. |

Total Maryland income tax, local income tax and contributions (Add lines 21 through 25.). |

26. |

|||||

27. |

Maryland and local tax withheld. See Instruction 17 |

. . . |

. . . . . . . . . . . |

27. |

|||

28.Estimated tax payments and payments made with extension request and

with Form MW506NRS.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .  28.

28.

29.Nonresident tax paid by

(Attach Maryland Schedule  29.

29.

30.Refundable Business and/or Heritage Structure Rehabilitation tax credits

|

(Attach Form 504CR and/or Form 502S.) |

. . . . . . . . . . |

. |

. . . . . . . . . . |

|

30. |

||

31. |

Total payments and credits (Add lines 27 through 30.) |

. . . . . . . . . . |

|

31. |

||||

32. |

Balance due (If line 26 is more than line 31, enter the difference.) |

. . . . . . . . . . |

|

32. |

||||

33. |

Overpayment (If line 26 is less than line 31, enter the difference.) |

. . . . . . . . . . |

|

33. |

||||

34. Amount of overpayment to be applied to 2023 estimated tax |

34. |

|||||||

35. |

.. . . . . . .Amount of overpayment to be refunded (Subtract line 34 from line 33.) |

REFUND |

|

35. |

||||

36. |

Interest charges from Form 504UP |

|

or for late filing |

|

|

. . . . Total |

36. |

|

|

|

|||||||

37. |

TOTAL AMOUNT DUE (Add lines 32 and 36.) |

. . . . . . . . . . |

. |

. . . . . . . . . . |

|

37. |

||

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.

.

.

.

.

.

.

.

.

.

.

AMENDED RETURNS

If you are filing an amended fiduciary income tax return, check the applicable boxes and draw a line through any bar codes on the front. Explain the changes you are making in the space below. Attach a copy of the amended federal Form 1041 if the federal return is being amended, and any other required documentation.

________________________________________________________________________________________________________

________________________________________________________________________________________________________

________________________________________________________________________________________________________

________________________________________________________________________________________________________

________________________________________________________________________________________________________

________________________________________________________________________________________________________

|

|

MARYLAND |

FIDUCIARY INCOME |

2022 |

||

|

|

|

|

|

|

|

|

|

FORM |

TAX RETURN |

page 3 |

||

|

||||||

504 |

|

|

|

|

||

NAME |

|

|

FEIN |

|

|

|

|

|

|

|

|||

________________________________________________________________________________________________________

DIRECT DEPOSIT OF REFUND (see Instruction 18)

Verify that all account information is correct and clearly legible. If you are requesting direct deposit of your refund, com- plete the following. For Splitting Direct Deposit, use Form 588.

Check here if this refund will go to an account outside of the United States.

Check here if you authorize the State of Maryland to issue your refund by direct deposit.

38.For the direct deposit option, complete the following information clearly and legibly:

38a. |

Type of account: |

38a. |

|

Checking |

|

Savings |

||

38b. |

Routing Number |

38b. |

|

|

|

|

|

|

38c. |

Account number: |

38c. |

|

|

|

|

|

|

38d. |

Name(s) as it appears on the bank account |

. 38d. |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

SIGNATURE AND VERIFICATION

Check here

if you authorize your preparer to discuss this return with us.

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements and to the best of my knowledge and belief it is true, correct and complete. If prepared by a person other than taxpayer, the declaration is based on all information of which the preparer has any knowledge.

Signature of Fiduciary or Officer representing Fiduciary |

Date |

Printed name of the Preparer / or Firm's name |

|

Street address of Preparer or Firm's address

City, State, ZIP Code + 4

Signature of preparer other than fiduciary (Required by Law) |

Date |

Telephone number of preparer |

Preparer’s PTIN (Required by Law) |

Daytime telephone number (Fiduciary)

CODE NUMBERS (3 digits per line)

Nonresidents must include Form 504NR.

Make checks payable to and mail to:

Comptroller Of Maryland

Revenue Administration Division

110 Carroll Street

Annapolis, Maryland

(Write Your Federal Employer Identification Number On Check Using Blue Or Black Ink.)

Not including the correct federal employer identification number: This number is essential for identifying the estate or trust. Make sure it’s accurate.

Failing to check the appropriate type of entity: Select the correct box for decedent’s estate, simple trust, complex trust, or any other type. This affects how the form is processed.

Incorrectly marking resident status: Be sure to check the right box indicating whether you are a resident or nonresident. This impacts tax calculations.

Omitting necessary signatures: Both the fiduciary and any preparer must sign the form. Without signatures, the return may be deemed incomplete.

Not attaching required documentation: If you’re claiming deductions or credits, attach the necessary forms, like Schedule K-1 for nonresident beneficiaries.

Failing to check for final return status: If this is the final return for the estate or trust, make sure to check the box indicating that.

Inaccurate calculations for Maryland modifications: Ensure that the figures for additions and subtractions are correct. Mistakes here can lead to incorrect tax amounts.

Missing the direct deposit information: If you want your refund directly deposited, fill out the account information accurately. Double-check the routing and account numbers.

Not providing an explanation for amended returns: If you’re filing an amended return, include a clear explanation of the changes made. This helps the processing of your return.

What is the Maryland 504 form?

The Maryland 504 form is a fiduciary income tax return used by estates and trusts in Maryland. It is essential for reporting the income earned by the estate or trust during a specific tax year. This form helps determine the taxable income and the tax liability for the fiduciary responsible for managing the estate or trust assets. It is important for ensuring compliance with state tax regulations.

Who needs to file the Maryland 504 form?

Fiduciaries of decedent estates, simple trusts, complex trusts, grantor-type trusts, bankruptcy estates, and qualified funeral trusts are required to file the Maryland 504 form. If the estate or trust has generated income during the tax year, the fiduciary must report this income using the form. Additionally, if the estate or trust is closing, a final return must be filed.

What information is required to complete the Maryland 504 form?

To complete the Maryland 504 form, you will need the federal employer identification number, the name and address of the estate or trust, and details about the fiduciary. For decedent estates, the date of death and the decedent's Social Security number are also necessary. Furthermore, you will need to provide information on income, deductions, and any modifications specific to Maryland tax regulations.

How do I determine if I need to file an amended Maryland 504 form?

If you discover errors or omissions after submitting the original Maryland 504 form, you should file an amended return. Indicate that it is an amended return by checking the appropriate box on the form. Ensure you include an explanation of the changes you are making and attach any required documentation, such as a copy of the amended federal Form 1041 if applicable.

What are Maryland modifications, and how do they affect the return?

Maryland modifications refer to specific adjustments that affect the taxable income of the estate or trust. These modifications may include additions, such as interest on state and local obligations, and subtractions, such as income from U.S. obligations. Understanding these modifications is crucial, as they directly impact the calculation of Maryland adjusted gross income and, ultimately, the tax owed.

What is the nonresident beneficiary deduction?

The nonresident beneficiary deduction applies when any beneficiaries of the estate or trust are not residents of Maryland. This deduction allows for the exclusion of income from intangible personal property accumulated for nonresident beneficiaries. To claim this deduction, you must complete the relevant section of the Maryland 504 form and attach Form 504 Schedule K-1 for each nonresident beneficiary.

How is the tax calculated on the Maryland 504 form?

The tax calculation on the Maryland 504 form involves determining the Maryland taxable net income of the fiduciary. This is done by subtracting any claimed exemptions from the Maryland adjusted gross income. The resulting figure is then used to calculate the Maryland tax owed based on the applicable tax rate schedule. Local or special nonresident taxes may also apply, depending on the circumstances.

What should I do if I have an overpayment or balance due?

If your calculations show an overpayment, you can choose to have the amount refunded or applied to your estimated tax for the following year. Conversely, if you have a balance due, it is essential to pay this amount by the due date to avoid penalties and interest. The form provides clear lines for indicating overpayments and balances due, making it straightforward to manage your tax obligations.