Fill Out Your Maryland 500E Template

Fill Out Your Maryland 500E Template

When filling out the Maryland 500E form, it is essential to follow certain guidelines to ensure your application is processed smoothly. Here are some dos and don'ts to keep in mind:

Understanding the Maryland 500E form is crucial for corporations seeking an extension on their income tax return. However, several misconceptions can lead to confusion and potential issues. Here are four common misunderstandings:

This is not true. While the 500E form does extend the time to file the tax return, it does not extend the time to pay any taxes owed. Corporations must remit full payment with the form to avoid penalties and interest.

Submitting the form does not guarantee an extension. If the application is not completed correctly or if payment is insufficient, the extension request may be denied. It is essential to follow all instructions carefully to ensure approval.

This is incorrect. The Maryland 500E form is specifically designed for C corporations. S corporations must use a different form, known as Form 510, to request an extension.

This is a misunderstanding of the purpose of the form. Corporations may seek an extension for various reasons, including needing more time to prepare accurate financial statements. Regardless of the reason, it is important to file the extension application timely.

Real Estate Addendum Template - Information regarding reforestation requirements may be necessary if the property has a significant land area.

For those navigating real estate transactions in Ohio, utilizing the Ohio Payoff form is essential. This document aids in acquiring necessary debt information from the State of Ohio, which is particularly important when dealing with properties that have outstanding liens. To facilitate this process, one can refer to resources such as Ohio PDF Forms for guidance on how to correctly complete and submit the form, ensuring compliance with state regulations.

Md 510 Instructions 2023 - Keep accurate records of filing and payments for future reference or inquiries.

Here are key takeaways regarding the Maryland 500E form:

After completing the Maryland 500E form, it must be submitted to the Comptroller of the Treasury by the specified deadline. Ensure that all required information is accurate and that the necessary payment accompanies the form. This application will allow the corporation to request an extension for filing the income tax return.

M ARYLAND |

|

APPLICATION FOR EXTENSION OF TIME TO |

|

|

|

19 |

|

||||||||||

FORM 500E |

|

FILE CORPORATION INCOME TAX RETURN |

|

|

|

|

|||||||||||

(Revised 1996) |

|

|

FOR TAXABLE YEAR BEGINNING_____________, 19___ |

|

|

|

|

||||||||||

|

M AIL TO: |

COM PTROLLER OF THE TREASURY |

ENDING_____________, 19___ |

|

|

|

|

|

|

||||||||

|

|

REVENUE ADM INISTRATION DIVISION |

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

ANNAPOLIS, M ARYLAND |

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

DO NOT WRITE IN THIS SPACE |

|||||||||||

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Nam e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Num ber and street |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

RM |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City or tow n |

|

|

|

State |

Zip code |

|

M E |

YE |

|

EC |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

▶ |

▶ |

|

▶ |

|

▶ |

|

▶ |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Federal Em ployer Identification No. (9 digits) |

|

FEIN Applied for date |

|

Date of Incorporation (6 digits) |

|

|

Federal Business Code No. (4 digits) |

|||||||||

|

▶ |

|

|

|

|

|

|

▶ |

|

|

|

|

|

▶ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CHECK HERE IF: |

|

☐ NAME OR ADDRESS HAS CHANGED |

NOTE: DO NOT USE THIS FORM |

) |

|

|

|

|

|||||||||

|

FOR S CORPORATIONS — SEE |

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

☐ FIRST FILING OF THE CORPORATION |

(INSTRUCTIONS FOR FORM 510 |

|

|

|

|

|||||||||

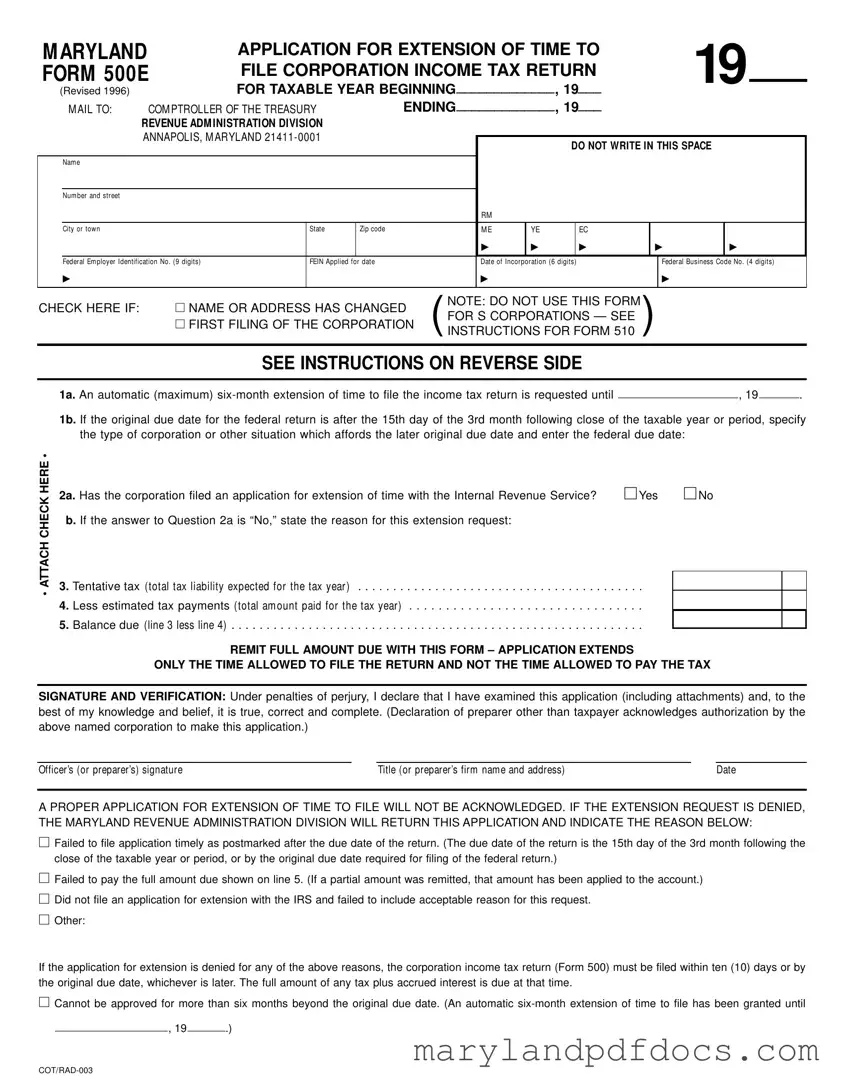

SEE INSTRUCTIONS ON REVERSE SIDE

• ATTACH CHECK HERE •

1a. An automatic (maximum)

1b. If the original due date for the federal return is after the 15th day of the 3rd month following close of the taxable year or period, specify the type of corporation or other situation which affords the later original due date and enter the federal due date:

2a. Has the corporation filed an application for extension of time with the Internal Revenue Service? |

☐ Yes |

☐ No |

0b. If the answer to Question 2a is “No,” state the reason for this extension request:

3. Tentative tax (total tax liability expected for the tax year ) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

4. Less estimated tax payments (total am ount paid for the tax year) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

5. Balance due (line 3 less line 4) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

REMIT FULL AMOUNT DUE WITH THIS FORM – APPLICATION EXTENDS

ONLY THE TIME ALLOWED TO FILE THE RETURN AND NOT THE TIME ALLOWED TO PAY THE TAX

SIGNATURE AND VERIFICATION: Under penalties of perjury, I declare that I have examined this application (including attachments) and, to the best of my knowledge and belief, it is true, correct and complete. (Declaration of preparer other than taxpayer acknowledges authorization by the above named corporation to make this application.)

Officer’s (or preparer’s) signature |

Title (or preparer’s firm nam e and address) |

Date |

A PROPER APPLICATION FOR EXTENSION OF TIME TO FILE WILL NOT BE ACKNOWLEDGED. IF THE EXTENSION REQUEST IS DENIED, THE MARYLAND REVENUE ADMINISTRATION DIVISION WILL RETURN THIS APPLICATION AND INDICATE THE REASON BELOW:

☐Failed to file application timely as postmarked after the due date of the return. (The due date of the return is the 15th day of the 3rd month following the close of the taxable year or period, or by the original due date required for filing of the federal return.)

☐Failed to pay the full amount due shown on line 5. (If a partial amount was remitted, that amount has been applied to the account.)

☐Did not file an application for extension with the IRS and failed to include acceptable reason for this request.

☐Other:

If the application for extension is denied for any of the above reasons, the corporation income tax return (Form 500) must be filed within ten (10) days or by the original due date, whichever is later. The full amount of any tax plus accrued interest is due at that time.

☐Cannot be approved for more than six months beyond the original due date. (An automatic

__________________, 19 ______.)

INSTRUCTIONS FOR MARYLAND FORM 500E (Revised 1996)

APPLICATION FOR EXTENSION OF TIME

TO FILE CORPORATION INCOME TAX RETURN

GENERAL INSTRUCTIONS

Purpose of Form Form 500E is used by a corporation to request an extension of time to file the corporation income tax return (Form 500) and to remit any balance of tax due.

NOTE: Do not use this form for

General Requirements Maryland law provides for an extension of time to file, but in no case can an extension be granted for more than six months beyond the original due date. A request for exten- sion of time to file will be automatically granted for six months, provided that:

1)Form 500E is properly filed and submitted by the original due date (15th day of the 3rd month following close of the tax year or period, or by the original due date required for filing of the federal return);

2)full payment of any balance due is submitted with Form 500E; and

3)an application for extension of time has been filed with the Internal Revenue Service or an acceptable reason has been provided with Form 500E.

A proper application for extension of time to file will not be acknowledged. If the extension request is denied, the corporation will be notified.

Form 500E does not extend the time allowed to pay the tax. Maryland law provides for accrual of interest and imposition of penalty for failure to pay any tax when due.

Consolidated returns are not allowed under Maryland law. Affiliated corporations which file a consolidated federal return must file separate Maryland extension applications for each member corporation.

When and Where to File File Form 500E by the 15th day of the 3rd month following the close of the taxable year or period, or by the original due date required for filing the federal return. The application for extension of time must be filed with the Comptroller of the Treasury, Revenue Administration Division, Annapolis, Maryland

SPECIFIC INSTRUCTIONS

Name, Address and Other Information Type or print the required information in the designated area. DO NOT USE THE LABEL FROM THE TAX BOOKLET COVER.

Enter the name exactly as specified in the Articles of Incorpo- ration, or as amended, and continue with any “Trading As” (T/A) name if applicable.

Enter the Federal Employer Identification Number (FEIN). If a FEIN has not been secured, enter “APPLIED FOR” followed by the date of application. If a FEIN has not been applied for, do so immediately.

Check the applicable box if the name or address has changed or if this is the first filing of the corporation.

Taxable Year or Period ENTER THE BEGINNING AND END-

ING DATES OF THE TAXABLE YEAR IN THE SPACE PROVIDED AT THE TOP OF FORM 500E.

The same taxable year or period used for the federal return must be used for Form 500E.

Tentative Tax Enter the total amount of income tax liability expected for the tax year on line 3.

Estimated Tax Payments Enter on line 4 the total amounts paid with Form 500DP or 500D – Declaration of Estimated Corporation Income Tax for the taxable year or period. Also include any amount carried forward as a credit from the prior year Form 500 – Corporation Income Tax Return.

Balance Due Enter the amount of tax due on line 5 and remit full payment with this form.

Signature and Verification An authorized officer or the paid preparer must sign and date Form 500E indicating the corporate title or preparer firm name and address.

Payment Instructions Include a check or money order made payable to the Comptroller of the Treasury for the full amount of any balance due. All payments must indicate the Federal Employer Identification Number, type of tax and tax year beginning and ending dates. DO NOT SEND CASH.

Mailing Instructions Use the envelope provided in the tax booklet and place an “X” in the appropriate box in the lower left corner to indicate the type of document enclosed. Also, be sure to read and follow the reminders listed on the back of the envelope.

Incorrect Dates: Failing to accurately enter the beginning and ending dates of the taxable year can lead to confusion. The dates must align with those used in the federal return.

Missing Federal Employer Identification Number (FEIN): Omitting the FEIN or writing “Applied For” without the application date can result in processing delays. If a FEIN has not been secured, it should be applied for immediately.

Improper Payment Submission: Not including the full amount due with the form is a common error. The application extends only the time to file, not the time to pay taxes owed.

Failure to Check Required Boxes: Neglecting to check the appropriate boxes regarding name or address changes can lead to complications. This information is crucial for accurate processing.

Signature Issues: Submitting the form without the required signature or date can cause the application to be deemed invalid. An authorized officer must sign the form.

Not Filing with the IRS: If a corporation has not filed an extension request with the IRS, it must include an acceptable reason for the Maryland request. Failure to do so can result in denial of the extension.

What is the Maryland 500E form?

The Maryland 500E form is an application for an extension of time to file a corporation income tax return in Maryland. It allows corporations to request an automatic six-month extension, provided certain conditions are met. This form must be submitted by the original due date of the tax return.

Who should use the Maryland 500E form?

This form is specifically for corporations that need additional time to file their income tax returns. It is important to note that this form should not be used by S corporations or for employer withholding tax purposes.

What are the requirements to obtain an extension using the Maryland 500E form?

To qualify for the extension, the following conditions must be met: the form must be properly filed by the original due date, full payment of any tax balance due must accompany the form, and an application for extension must have been filed with the IRS or a valid reason for the extension must be provided.

When is the Maryland 500E form due?

The form must be filed by the 15th day of the 3rd month following the close of the corporation's taxable year or by the original due date required for filing the federal return. Missing this deadline may result in denial of the extension.

What happens if the extension request is denied?

If the extension request is denied, the corporation must file the income tax return within ten days of the denial or by the original due date, whichever is later. Any tax due, along with accrued interest, must be paid at that time.

Can I file a consolidated return for multiple corporations using the Maryland 500E form?

No, Maryland law does not allow consolidated returns. Each affiliated corporation that files a consolidated federal return must submit a separate Maryland 500E form to request an extension.

How should I submit payment with the Maryland 500E form?

Include a check or money order made payable to the Comptroller of the Treasury for the full amount of any balance due. Ensure that the payment includes the Federal Employer Identification Number, the type of tax, and the beginning and ending dates of the tax year. Do not send cash.