Fill Out Your Maryland 500Dm Template

Fill Out Your Maryland 500Dm Template

When filling out the Maryland 500DM form, it is essential to follow specific guidelines to ensure accuracy and compliance. Here are five important dos and don'ts to keep in mind:

Misconceptions about the Maryland 500Dm form can lead to confusion and errors in tax filing. Below is a list of common misconceptions along with clarifications to help taxpayers understand the form better.

Maryland Personal Property Tax - Completing the form accurately is crucial for tax compliance in Maryland.

Understanding the complexities of a business Loan Agreement is crucial for any entrepreneur seeking financing. This document serves not only to protect both the lender and the borrower but also clarifies expectations related to the loan terms.

What Does I Claim Exemption From Withholding Mean - The MW507 helps to balance tax withholding and refund expectations throughout the year.

What Is a Certificate of Compliance Maryland - Business entities are encouraged to keep abreast of developments in workers' compensation law to ensure continued compliance.

Here are key takeaways about filling out and using the Maryland 500Dm form:

Completing the Maryland 500DM form involves several steps to ensure accurate reporting of modifications related to federal tax provisions. After filling out the form, you will need to attach it to your Maryland income tax return or amended return as appropriate.

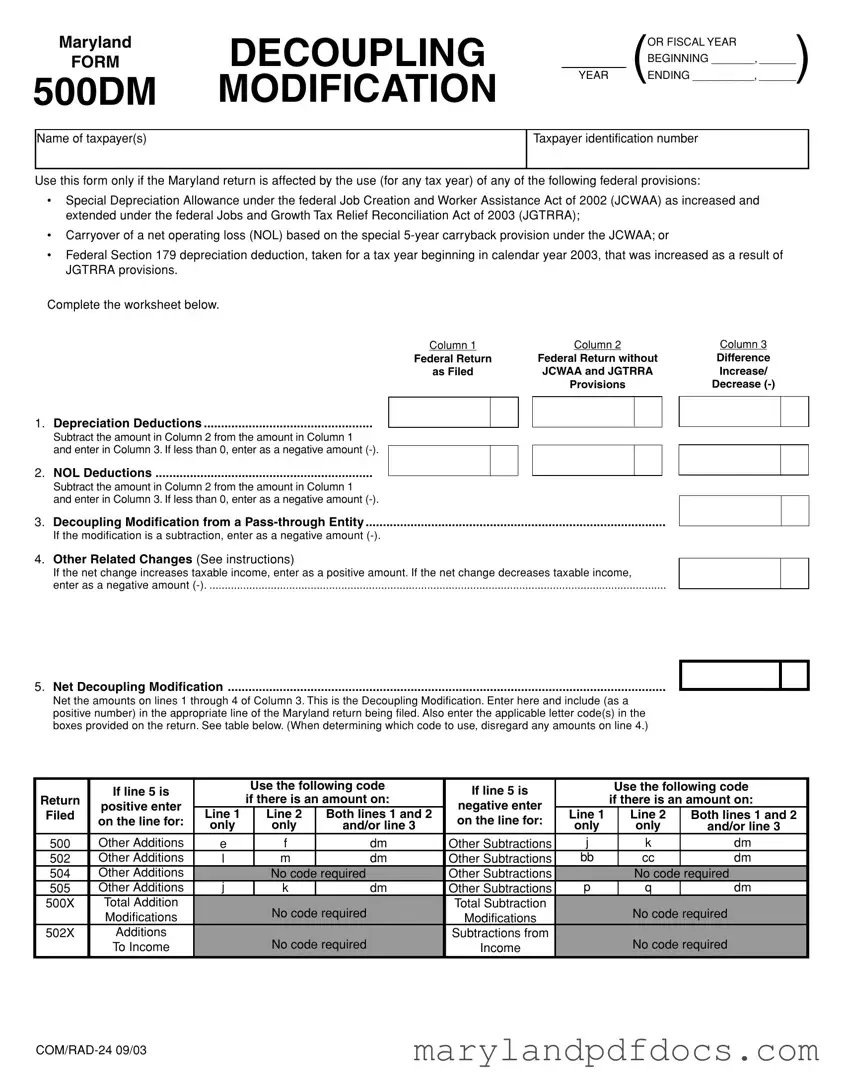

Maryland |

DECOUPLING |

YEAR |

OR FISCAL YEAR |

FORM |

_ (ENDING __________, ______) |

||

|

|

|

BEGINNING _______, ______ |

500DM |

MODIFICATION |

|

|

Name of taxpayer(s)

Taxpayer identification number

Use this form only if the Maryland return is affected by the use (for any tax year) of any of the following federal provisions:

•Special Depreciation Allowance under the federal Job Creation and Worker Assistance Act of 2002 (JCWAA) as increased and extended under the federal Jobs and Growth Tax Relief Reconciliation Act of 2003 (JGTRRA);

•Carryover of a net operating loss (NOL) based on the special

•Federal Section 179 depreciation deduction, taken for a tax year beginning in calendar year 2003, that was increased as a result of JGTRRA provisions.

Complete the worksheet below.

Column 1 |

Column 2 |

Column 3 |

Federal Return |

Federal Return without |

Difference |

as Filed |

JCWAA and JGTRRA |

Increase/ |

|

Provisions |

Decrease |

1. Depreciation Deductions .................................................

Subtract the amount in Column 2 from the amount in Column 1

and enter in Column 3. If less than 0, enter as a negative amount

2.NOL Deductions ...............................................................

Subtract the amount in Column 2 from the amount in Column 1

and enter in Column 3. If less than 0, enter as a negative amount

3.Decoupling Modification from a

If the modification is a subtraction, enter as a negative amount

4.Other Related Changes (See instructions)

If the net change increases taxable income, enter as a positive amount. If the net change decreases taxable income,

enter as a negative amount

5.Net Decoupling Modification ...............................................................................................................................

Net the amounts on lines 1 through 4 of Column 3. This is the Decoupling Modification. Enter here and include (as a positive number) in the appropriate line of the Maryland return being filed. Also enter the applicable letter code(s) in the boxes provided on the return. See table below. (When determining which code to use, disregard any amounts on line 4.)

|

If line 5 is |

|

Use the following code |

If line 5 is |

|

Use the following code |

||||

Return |

|

if there is an amount on: |

|

if there is an amount on: |

||||||

positive enter |

|

negative enter |

|

|||||||

Filed |

Line 1 |

|

Line 2 |

Both lines 1 and 2 |

Line 1 |

|

Line 2 |

Both lines 1 and 2 |

||

on the line for: |

|

on the line for: |

|

|||||||

|

only |

|

only |

and/or line 3 |

only |

|

only |

and/or line 3 |

||

|

|

|

|

|

||||||

500 |

Other Additions |

e |

|

f |

dm |

Other Subtractions |

j |

|

k |

dm |

502 |

Other Additions |

l |

|

m |

dm |

Other Subtractions |

bb |

|

cc |

dm |

504 |

Other Additions |

|

|

No code required |

Other Subtractions |

|

|

No code required |

||

505 |

Other Additions |

j |

|

k |

dm |

Other Subtractions |

p |

|

q |

dm |

500X |

Total Addition |

|

|

No code required |

Total Subtraction |

|

|

No code required |

||

|

Modifications |

|

|

Modifications |

|

|

||||

502X |

Additions |

|

|

No code required |

Subtractions from |

|

|

No code required |

||

|

To Income |

|

|

Income |

|

|

||||

INSTRUCTIONS FOR |

PAGE 2 |

MARYLAND FORM 500DM |

|

DECOUPLING MODIFICATION

General Instructions

Purpose of Form

Maryland has decoupled from certain federal provisions, as listed at the top of Form 500DM, by enacting addition and subtraction modifications which eliminate the effect of the changes on Maryland and local taxes. This form is used to determine the amount of the required modification.

Use of Pro Forma Returns

Separate (pro forma) federal and Maryland returns must be prepared for use in completing Form 500DM. In addition to calculating depreciation and NOL deductions without the benefits afforded under the Job Creation and Worker Assistance Act of 2002 (JCWAA) and the Jobs and Growth Tax Relief Reconciliation Act of 2003 (JGTRRA), pro forma returns will also help to determine other related items that affect Maryland and local income tax liability (e.g., income items, addition and subtraction modifications, deductions and credits).

Additional Information

For more information regarding these modifications, see Administrative Release 38 which is available on our website at www.marylandtaxes.com or from any office of the Comptroller.

Specific Instructions

Column 1 – Federal Return as Filed

Column 1 (lines 1 and 2) is used for the amounts reported on the federal return which include the impacts of the Special Depreciation Allowance, the special

Column 2 – Federal Return Without JCWAA and JGTRRA Provisions

Examples of items affected by decoupling are:

¥Gain or loss on sale of property

¥Recapture of depreciation

¥Passive loss

¥Maryland itemized deductions

Line 5 – Total

Net the amounts from lines 1 through 4 and enter on line 5. If line 5 is positive, include this amount in the appropriate line of the Maryland tax return being filed. Also enter the appropriate code letter(s) in the box(es) provided for the type of addition modification (either depreciation or NOL, or both).

If line 5 is negative, include this amount as a positive number in the appropriate line of the Maryland tax return being filed. Enter the appropriate code letter(s) in the box(es) provided for the type of subtraction modification (either depreciation or NOL, or both).

See the table at the bottom of Form 500DM for the line numbers and code letters to use.

Credits

For Maryland income tax credits affected by electing JCWAA and/or JGTRRA treatment, enter on the return to be filed, credits as calculated on the Maryland pro forma return without JCWAA and/or JGTRRA treatment.

Note: If a credit for a tax paid to another state was claimed on the original return and the tax liability to the other state and/or Maryland changes as a result of the treatment of the JCWAA and/or JGTRRA provisions in either state, a revised Form 502CR must be completed using the Maryland and the other stateÕs returns to be filed including all amendments and modifications.

Column 2 (lines 1 and 2) is for the amounts which would have been reported on the federal return using federal law in effect prior to enactment of the JCWAA and JGTRRA (without regard to the Special Depreciation Allowance, the special

Column 3 – Change – increase/decrease

Lines 1 and 2 — Subtract the amount in Column 2 from the amount in Column 1. Enter in Column 3. Line 4 is for the change to taxable income in other related items (calculated before and after application of the JCWAA and JGTRRA provisions) that would affect taxable income. If the change decreases taxable income, enter the amount with a minus sign

Line 1 – Depreciation Deductions

Use line 1 only for the depreciation expense deductions.

Line 2 – NOL Deductions

Use line 2 for NOL deductions. For Columns 1 and 2, limit the deductions as follows: For a corporation, the deduction may not exceed the federal taxable income. For all others, the deduction may not exceed the federal modified taxable income as determined on federal Form 1045, Schedule B.

Line 3 – Decoupling Modification from a

Use line 3 for decoupling modifications reported by a

Line 4 – Other Related Changes

If the entity is a PTE (partnership,

Income from a PTE

Each partner, shareholder or member that has a decoupling modification from a PTE must also complete Form 500DM. Enter the decoupling modification from the PTE on line 3 of Form 500DM. Also use this amount to adjust the income from the PTE on the pro forma federal return to determine if other related changes exist. These changes would be entered on line 4 of Form 500DM. Do not include any decoupling modification on the Maryland pro forma return.

Attachment of Forms

¥Original Return Attach the completed Form 500DM to the Maryland income tax return to be filed. Pro forma returns used to complete this form are not to be filed with the Comptroller or the IRS, but should be retained with your tax records.

¥Amended Return Attach the completed Form 500DM, schedules and pro forma returns to amended return to be filed.

For questions concerning Form 500DM contact:

Revenue Administration Division

Annapolis, Maryland

www.marylandtaxes.com

Decoupling may also affect other items included in federal adjusted gross income (AGI) allowable itemized deductions, as well as Maryland addition and subtraction modifications. Because these items also affect Maryland taxable income, the decoupling modification must include an adjustment for these changes. If the net change for these items reduces taxable income, enter as a negative amount

07/03

Not using pro forma returns: Many individuals fail to prepare separate federal and Maryland pro forma returns. These are essential for accurately completing the 500DM form.

Incorrectly filling out columns: Some people mistakenly enter amounts in the wrong columns. Ensure that Column 1 reflects the federal return as filed, while Column 2 should show the federal return without the JCWAA and JGTRRA provisions.

Ignoring negative amounts: When calculating changes, individuals often overlook the need to enter negative amounts correctly. If a deduction decreases taxable income, it should be marked with a minus sign (-).

Missing required codes: Failing to include the appropriate code letters for additions or subtractions on the Maryland return can lead to processing delays or errors. Always refer to the table provided on the form.

Not attaching the form: Some taxpayers forget to attach the completed 500DM form to their Maryland income tax return. This is a crucial step that should not be skipped.

Overlooking the decoupling modification: Individuals may fail to net the amounts from lines 1 through 4 correctly. This total is essential for determining the final decoupling modification amount.

Confusing line items: Misunderstanding which line items to report can lead to mistakes. Each line has specific instructions that must be followed closely to avoid errors.

What is the purpose of the Maryland 500Dm form?

The Maryland 500Dm form is designed to determine the decoupling modifications required for Maryland state taxes. This form is necessary when a taxpayer's Maryland return is influenced by certain federal tax provisions, such as the Special Depreciation Allowance or the carryover of a net operating loss. By completing this form, taxpayers can eliminate the effects of these federal provisions on their Maryland tax liability, ensuring that they comply with state tax regulations.

Who needs to file the Maryland 500Dm form?

How do I complete the Maryland 500Dm form?

To complete the Maryland 500Dm form, taxpayers should first prepare separate federal and Maryland pro forma returns. This allows for accurate calculations of depreciation and net operating loss deductions without the federal benefits. The form requires entering amounts from the federal return as filed and then determining the differences caused by the decoupling provisions. The form includes a worksheet to help calculate the necessary modifications, which will ultimately be reported on the Maryland tax return.

What should I do if I have a decoupling modification from a pass-through entity?

If you are a partner, shareholder, or member of a pass-through entity that has a decoupling modification, you must also complete the 500Dm form. You will report your share of the modification on line 3 of the form. It is essential to include this amount when adjusting your income from the pass-through entity on your pro forma federal return. This ensures that any related changes affecting taxable income are accurately reflected.

Where can I find more information about the Maryland 500Dm form?

Additional information regarding the Maryland 500Dm form can be found on the Maryland Comptroller's website or by contacting their Revenue Administration Division. They provide resources, guidelines, and answers to frequently asked questions to assist taxpayers in navigating the decoupling modifications and the completion of the form. This support is crucial for ensuring compliance and understanding how federal provisions impact state tax responsibilities.