Fill Out Your Maryland 4B Template

Fill Out Your Maryland 4B Template

When filling out the Maryland 4B form, it is essential to approach the task with care. Here are ten important do's and don'ts to keep in mind:

By following these guidelines, you can navigate the Maryland 4B form with greater confidence and accuracy.

Here are some common misconceptions about the Maryland 4B form:

Mw506nrs - Timeliness is key; the form must be submitted 21 days before the closing date.

Completing the Ohio Payoff form accurately is essential for realtors and title companies to facilitate property transactions smoothly. By utilizing resources such as Ohio PDF Forms, individuals can ensure they have the correct information and guidelines needed to clear liens and comply with state regulations effectively.

Maryland 502 - Each completed form is a record of judicial actions taken in response to noncompliance.

Maryland Form 502 Instructions - Fiduciaries must provide their federal employer identification number on the Maryland 504 form.

When filling out the Maryland Form 4B, it is essential to understand the details required for accurate reporting. Here are some key takeaways to keep in mind:

Being thorough and attentive to detail when filling out the Maryland Form 4B is crucial for compliance and accurate financial reporting. Take the time to review each section carefully.

Completing the Maryland Form 4B is an important step for organizations that own property in Maryland. This form helps track depreciation and report property details accurately. To ensure compliance, follow the steps outlined below carefully.

After completing these steps, your form will be ready for submission. It is essential to keep a copy for your records. If you have any questions or need assistance during the process, consider reaching out to a qualified professional for guidance.

Maryland |

Depreciation Schedule |

|

Form 4B |

||

|

||

|

PROPERTY IN MARYlAND AS OF _____________________________ |

2012

Form 4B & 4C

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL |

|

|

DEPRECIATION |

|

|

ACCUMULATED |

|

BOOK |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

COST |

|

|

|

|

THIS YEAR |

|

|

DEPRECIATION |

|

VALUE |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1. |

|

|

Land |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. |

|

|

Building |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. |

|

|

Leasehold Improvements |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

4. |

|

|

Transportation Equipment (Registered)A |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5. |

|

|

Transportation Equipment |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

(Not Registered and Interchangeable Registrations) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6. |

|

|

Furniture & Fixtures |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7. |

|

|

Machinery & Equipment |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8. |

|

|

Other (Specify) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9. |

|

|

Totals:B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

10.Expensed Property |

(Not Reported on |

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

Depreciation Schedule) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

11. Exempt Personal PropertyD |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

(Included in line 9 above and not reported on the return.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

Type of Organization |

|

|

EXEMPTION CLAIMED |

|

|

Type of Property |

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

n |

Charitable |

|

n |

Religious |

|

|

|

|

|

n |

|

Vehicles (Registered) |

n |

Vessels (under 100 ft.) |

||||||||||

|

|

|

|

Veterans |

|

|

|

|

|

|

|

Aircraft |

|

|

|

|

|

|

||||||||

|

|

|

n |

|

Educational |

|

n |

|

|

|

|

|

n |

|

|

n |

Farming Implements (Farmers Only) |

|||||||||

|

|

n |

Other ___________________________________________ |

|

|

n |

Rental Heavy EquipmentE |

n |

Other_________________ |

|||||||||||||||||

|

|

|||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||

|

|

|

|

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|

SPECIFY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SPECIFY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

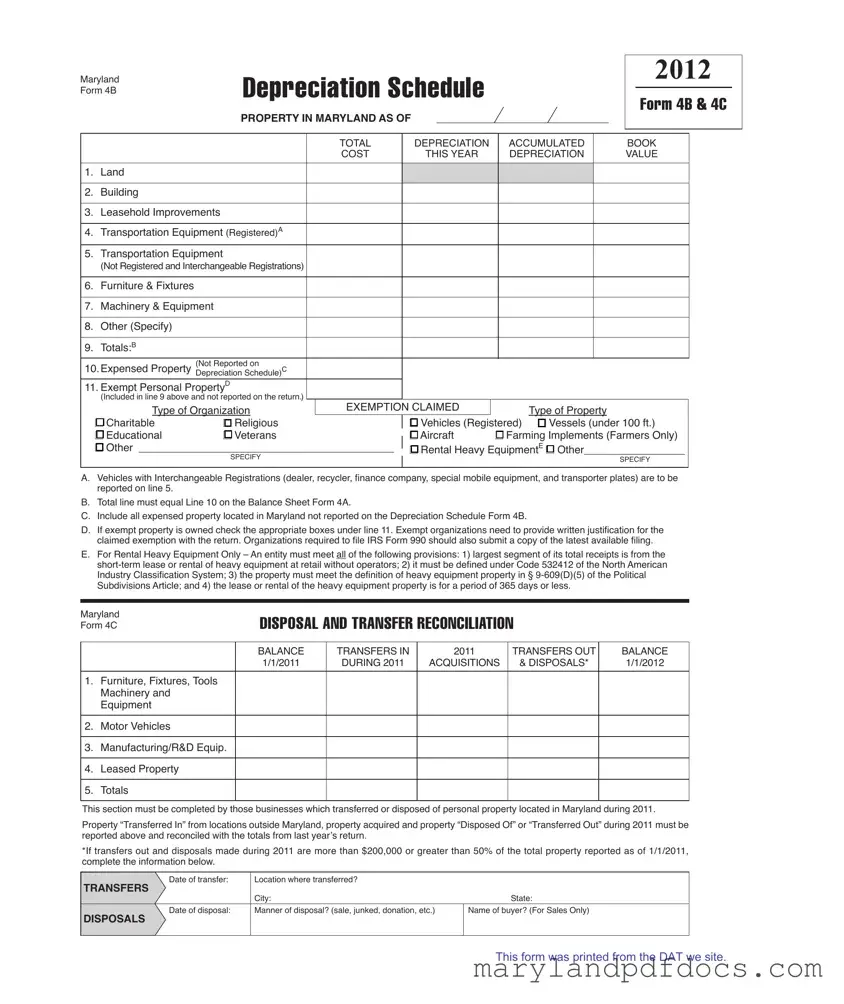

A.Vehicles with Interchangeable Registrations (dealer, recycler, finance company, special mobile equipment, and transporter plates) are to be reported on line 5.

B.Total line must equal Line 10 on the Balance Sheet Form 4A.

C.Include all expensed property located in Maryland not reported on the Depreciation Schedule Form 4B.

D.If exempt property is owned check the appropriate boxes under line 11. Exempt organizations need to provide written justification for the claimed exemption with the return. Organizations required to file IRS Form 990 should also submit a copy of the latest available filing.

E.For Rental Heavy Equipment Only – An entity must meet all of the following provisions: 1) largest segment of its total receipts is from the

Maryland Form 4C

DISPOSAL AND TRANSFER RECONCILIATION

|

|

BALANCE |

TRANSFERS IN |

2011 |

TRANSFERS OUT |

BALANCE |

|

|

1/1/2011 |

DURING 2011 |

ACQUISITIONS |

& DISPOSALS* |

1/1/2012 |

|

|

|

|

|

|

|

1. |

Furniture, Fixtures, Tools |

|

|

|

|

|

|

Machinery and |

|

|

|

|

|

|

Equipment |

|

|

|

|

|

|

|

|

|

|

|

|

2. |

Motor Vehicles |

|

|

|

|

|

|

|

|

|

|

|

|

3. |

Manufacturing/R&D Equip. |

|

|

|

|

|

|

|

|

|

|

|

|

4. |

Leased Property |

|

|

|

|

|

|

|

|

|

|

|

|

5. |

Totals |

|

|

|

|

|

|

|

|

|

|

|

|

This section must be completed by those businesses which transferred or disposed of personal property located in Maryland during 2011.

Property “Transferred In” from locations outside Maryland, property acquired and property “Disposed Of” or “Transferred Out” during 2011 must be reported above and reconciled with the totals from last year’s return.

*If transfers out and disposals made during 2011 are more than $200,000 or greater than 50% of the total property reported as of 1/1/2011, complete the information below.

Date of transfer: |

Location where transferred? |

|

TRANSFERS |

|

|

|

City: |

State: |

Date of disposal: |

Manner of disposal? (sale, junked, donation, etc.) |

Name of buyer? (For Sales Only) |

DISPOSAlS

This form was printed from the DAT we site.

Missing Information: Failing to fill in the date at the top of the form can lead to processing delays. Ensure that the property date is clearly indicated.

Incorrect Property Classification: Misclassifying property types can result in incorrect assessments. Each item must be categorized accurately according to the specified categories.

Omitting Exemptions: If claiming exemptions, it’s crucial to check the appropriate boxes and provide the necessary documentation. Neglecting this step can invalidate the exemption.

Inaccurate Totals: The total on line 9 must match the total reported on line 10 of Form 4A. Double-check calculations to avoid discrepancies.

Failure to Report Expensed Property: All expensed property located in Maryland must be included, even if it’s not on the depreciation schedule. Omitting this can lead to penalties.

Ignoring Transfer and Disposal Requirements: Businesses that have transferred or disposed of property must complete the relevant sections. Ignoring these requirements may result in incomplete filings.

Not Providing Justification for Exemptions: Exempt organizations must submit written justification for their claims. Failing to do so can lead to rejection of the exemption.

Incorrectly Reporting Rental Heavy Equipment: Ensure that all criteria for rental heavy equipment are met and documented. Misreporting can disqualify the property from exemptions.

What is the Maryland 4B form?

The Maryland 4B form is a Depreciation Schedule used by businesses to report the depreciation of personal property located in Maryland. It is essential for determining the taxable value of property and must be completed accurately to comply with state regulations.

Who needs to file the Maryland 4B form?

Any business or organization that owns personal property in Maryland and is subject to property tax must file the Maryland 4B form. This includes entities that own land, buildings, machinery, and equipment, among other types of property.

What types of property should be reported on the Maryland 4B form?

The form requires reporting various categories of property, including land, buildings, leasehold improvements, transportation equipment, furniture and fixtures, machinery and equipment, and any other specified property. Each category must be listed with its corresponding book cost and accumulated depreciation.

What is the purpose of the depreciation schedule?

The depreciation schedule serves to calculate the reduction in value of the reported assets over time. This information is crucial for determining the taxable value of the property and ensuring compliance with Maryland tax laws.

How is the total depreciation calculated on the form?

Total depreciation is calculated by summing the accumulated depreciation for each category of property reported on the Maryland 4B form. This total should match the corresponding line on the Balance Sheet Form 4A, ensuring consistency in financial reporting.

What exemptions are available on the Maryland 4B form?

Exemptions may be claimed for certain types of property, such as vehicles, vessels under 100 feet, and property owned by charitable, religious, or educational organizations. To claim an exemption, the appropriate boxes must be checked, and written justification must be provided with the return.

What is the significance of the expensed property section?

The expensed property section allows businesses to report property that has been expensed but not included in the depreciation schedule. This ensures that all property located in Maryland is accounted for, even if it does not qualify for depreciation.

What are the requirements for reporting rental heavy equipment?

To report rental heavy equipment, the business must derive the majority of its receipts from short-term leases of heavy equipment without operators. Additionally, the property must meet specific definitions outlined in the Maryland tax code, and the lease period must be 365 days or less.

What should businesses do if they transferred or disposed of property during the year?

Businesses that transferred or disposed of personal property during the year must complete the disposal and transfer reconciliation section of the Maryland 4B form. This includes reporting property transferred in, acquired, disposed of, or transferred out, along with relevant details such as dates and methods of disposal.

Where can businesses find more information about the Maryland 4B form?

Additional information about the Maryland 4B form, including instructions and guidelines for completion, can be found on the Maryland State Department of Assessments and Taxation website. It is advisable for businesses to consult this resource to ensure compliance with all filing requirements.