Fill Out Your 4A Maryland Template

Fill Out Your 4A Maryland Template

When filling out the 4A Maryland form, it's important to follow specific guidelines to ensure accuracy and compliance. Here are seven things you should and shouldn't do:

Understanding the 4A Maryland form is essential for businesses operating in the state. However, several misconceptions can lead to confusion. Here are nine common misunderstandings about the form:

Clearing up these misconceptions can help ensure that businesses accurately complete the 4A Maryland form and remain compliant with state regulations.

Daycare for Single Moms - There are options for students entering as freshmen, sophomores, juniors, seniors, or graduates.

State of Maryland Insurance - Failure to provide a completed form may result in claim denial.

The significance of having a Durable Power of Attorney form cannot be overstated, as it provides a means for individuals to ensure their wishes are respected when they may not be able to voice them. This essential legal document allows one to appoint someone trustworthy to manage their affairs, which is crucial in moments of incapacity. For those in Florida, utilizing a Durable Power of Attorney form is vital to navigate these circumstances while adhering to state laws, thus empowering individuals with peace of mind regarding their personal, financial, and healthcare decisions.

Maryland State Compliance Application - The Maryland State Compliance Application is essential for laboratory licensing in Maryland.

When filling out and using the 4A Maryland form, keep these key takeaways in mind:

Completing the 4A Maryland form is an essential task for businesses operating within the state. This form gathers financial information that helps in assessing the value of your business's personal property. To ensure accuracy and compliance, follow the steps outlined below carefully.

Once the form is filled out, it’s ready for submission. Make sure to keep a copy for your records before sending it to the appropriate department. This ensures you have documentation of your business’s financial standing for future reference.

STATE OF MARYLAND |

BALANCE SHEET |

2015 |

|

|

|

|

|

||

DEPARTMENT OFASSESSMENTSAND TAXATION |

|

|

|

|

PERSONAL PROPERTY DIVISION |

|

|

FORM 4A |

|

FORM 4A |

|

|

|

|

|

|

|

|

|

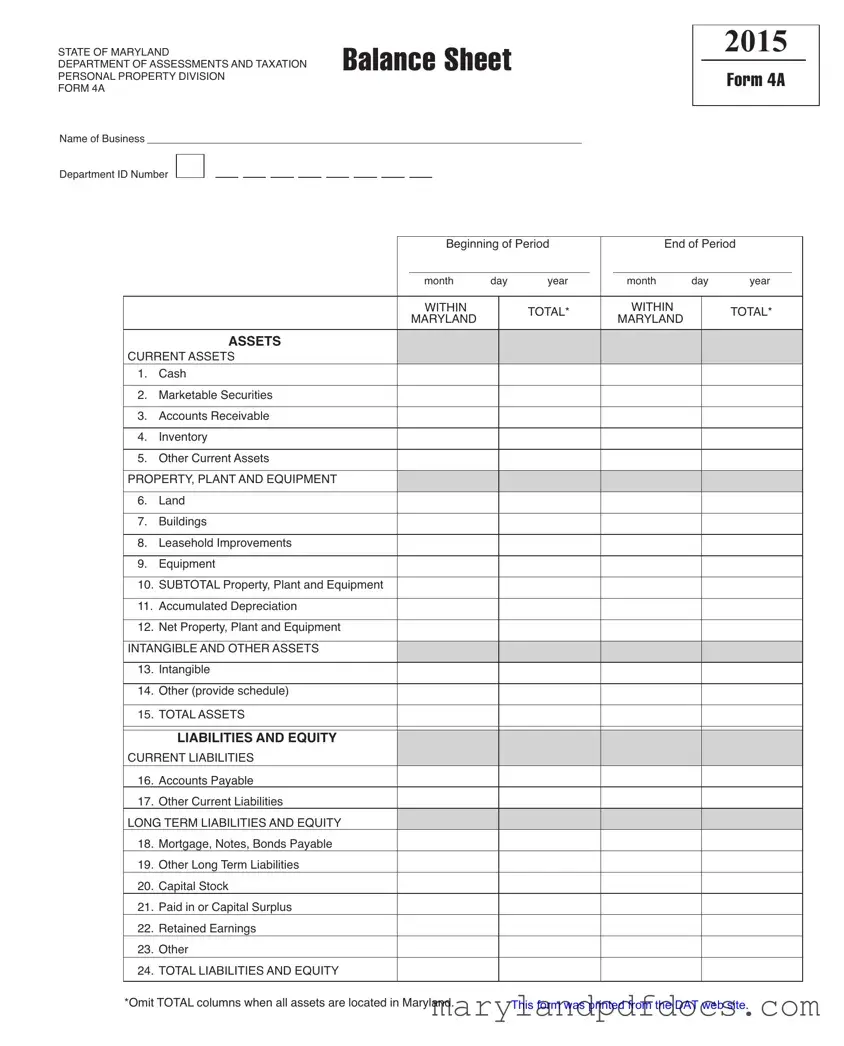

Name of Business__________________________________________________________________________

Department ID Number

|

|

Beginning of Period |

|

|

End of Period |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

month |

day |

year |

|

|

month |

day |

year |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

WITHIN |

|

|

|

|

|

WITHIN |

|

|

|

|

|

|

|

TOTAL* |

|

|

|

TOTAL* |

|

|

|||

|

|

MARYLAND |

|

|

|

|

MARYLAND |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|||

ASSETS

CURRENTASSETS

1.Cash

2.Marketable Securities

3.Accounts Receivable

4.Inventory

5.Other CurrentAssets

PROPERTY, PLANTAND EQUIPMENT

6.Land

7.Buildings

8.Leasehold Improvements

9.Equipment

10.SUBTOTAL Property, Plant and Equipment

11.Accumulated Depreciation

12.Net Property, Plant and Equipment

INTANGIBLEANDOTHERASSETS

13.Intangible

14.Other(provideschedule)

15.TOTALASSETS

LIABILITIESANDEQUITY

CURRENTLIABILITIES

16.AccountsPayable

17.OtherCurrentLiabilities

LONGTERMLIABILITIESANDEQUITY

18.Mortgage,Notes,BondsPayable

19.OtherLongTermLiabilities

20.CapitalStock

21.PaidinorCapitalSurplus

22.RetainedEarnings

23.Other

24.TOTALLIABILITIESANDEQUITY

*Omit TOTAL columns when all assets are located in Maryland.

This form was printed from the DAT web site.

Failing to provide the Name of Business clearly. This section is crucial for identification purposes.

Omitting the Department ID Number. Without this number, processing may be delayed.

Incorrectly reporting the Beginning of Period and End of Period dates. Ensure these dates accurately reflect the reporting period.

Neglecting to include all Current Assets. Items like cash, accounts receivable, and inventory must be accounted for to provide a complete picture.

Misclassifying Property, Plant, and Equipment. Each asset should be categorized correctly to avoid discrepancies.

Not calculating Accumulated Depreciation accurately. This figure is essential for determining the net value of assets.

Forgetting to list Intangible Assets. These can include patents or trademarks, which are important for a full financial assessment.

Leaving out Current Liabilities. Accounts payable and other liabilities must be reported to understand the company's obligations.

Ignoring the TOTAL LIABILITIES AND EQUITY section. This is vital for ensuring that the balance sheet is complete and accurate.

What is the 4A Maryland form?

The 4A Maryland form is a balance sheet used by businesses in Maryland to report their financial position. It provides a snapshot of a company's assets, liabilities, and equity at a specific point in time. This form is essential for the Department of Assessments and Taxation, particularly for personal property tax purposes.

Who needs to file the 4A Maryland form?

Any business operating in Maryland that holds personal property must file the 4A form. This includes sole proprietorships, partnerships, corporations, and limited liability companies (LLCs). If your business has assets located in Maryland, you are required to submit this form to ensure compliance with state regulations.

What information is required on the 4A Maryland form?

The form requires detailed information about your business's assets and liabilities. You’ll need to list current assets such as cash, accounts receivable, and inventory. Additionally, you must report property, plant, and equipment, including land and buildings, along with any accumulated depreciation. Finally, you will need to provide details on liabilities, including accounts payable and long-term debts, as well as equity components like capital stock and retained earnings.

When is the 4A Maryland form due?

The 4A form is typically due by April 15th each year. It’s important to keep this deadline in mind to avoid any potential penalties or interest charges. If you need more time, you may be able to request an extension, but be sure to check the specific guidelines provided by the Maryland Department of Assessments and Taxation.

What happens if I don’t file the 4A Maryland form?

Failing to file the 4A form can lead to penalties, including fines and interest on unpaid taxes. Additionally, your business may be subject to an estimated assessment, which could result in a higher tax bill. It’s crucial to stay compliant to avoid these unnecessary costs.

Can I amend my 4A Maryland form after filing?

Yes, you can amend your 4A form if you discover errors or omissions after submission. It’s advisable to correct any mistakes as soon as possible. You may need to provide documentation to support the changes. Contact the Maryland Department of Assessments and Taxation for guidance on the amendment process.

Is there a fee associated with filing the 4A Maryland form?

There is no fee for filing the 4A Maryland form itself. However, keep in mind that any taxes owed based on the information reported may still apply. Ensure that you calculate your tax liability accurately to avoid surprises.

Where can I find the 4A Maryland form?

The 4A Maryland form can be accessed online through the Maryland Department of Assessments and Taxation website. You can download a copy, fill it out, and submit it electronically or by mail, depending on your preference.

What if I have questions while filling out the 4A Maryland form?

If you have questions or need assistance while completing the form, you can reach out to the Maryland Department of Assessments and Taxation directly. They can provide guidance and clarify any aspects of the form that may be confusing. Additionally, consulting with a tax professional can be beneficial for more complex situations.